LSE DS202W 2025: Week 03 - Linear regression as a supervised learning algorithm

Linear regression as a machine learning algorithm

🥅 Learning Objectives

- Understand crucial differences between machine learning approaches and econometric analysis

- Understand the importance of training and test splits in our data

- Apply linear models using

scikit-learnandstatsmodels - Compare and contrast linear model performance with a penalised linear model

- Create clear visualisations of model performance

- Combine functions and list comprehensions to build multiple models

⚙️ Setup

Downloading the student notebook

Click on the below button to download the student notebook.

Loading libraries and functions

import numpy as np

import pandas as pd

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression, Lasso

from sklearn.metrics import r2_score, root_mean_squared_error

import statsmodels.api as sm

from lets_plot import *

LetsPlot.setup_html()Downloading the data

Download the dataset we will use for this lab, which is a dataset adapted from Wave 7 of the World Values Survey (Haerpfer et al. 2022). Use the link below to download this dataset:

Before we do anything more

Please create a data folder called data to store all the different data sets in this course.

The World Values Survey

wvs = pd.read_csv("data/wvs-wave-7.csv")

wvs = wvs.dropna()

print(wvs.shape)

(86867, 17)We start our machine learning journey with Wave 7 of the World Values Survey (wvs), which contains information on 86,867 individuals from 63 countries. We have cleaned the data to only include non-missing values. The columns include:

iso3c3-letter country iso codesatisfaction1 to 10 rating of life satisfaction (the outcome)social_trustTRUE / FALSE as to whether or not someone expresses social trustmalerespondent is male (reference: female)ageage of respondentpost_second_edurespondent has post-secondary educationruralrespondent lives in a rural area (reference: urban)employmentcategorical employment variable (trycount(wvs, employment))financial_situ1 to 10 rating of respondent’s financial situationmarriedthe respondent is married (reference: other marital status)relig_import1 to 10 rating of how much importance the respondent attaches to religion.better_livingtrichotomous rating of whether or not the respondent sees their lives as better off than their parents (trycount(wvs, better_living))no_food: In the last 12 months, how often have your or your family gone without enough food to eat? (Sometimes / Often = TRUE, Rarely / Never = FALSE)no_safetyIn the last 12 months, how often have your or your family felt unsafe from crime in your home? (Sometimes / Often = TRUE, Rarely / Never = FALSE)no_medicalIn the last 12 months, how often have your or your family gone without medicine or medical treatment that you needed? (Sometimes / Often = TRUE, Rarely / Never = FALSE)no_cashIn the last 12 months, how often have your or your family gone without a cash income? (Sometimes / Often = TRUE, Rarely / Never = FALSE)no_shelterIn the last 12 months, how often have your or your family gone without a safe shelter over your head? (Sometimes / Often = TRUE, Rarely / Never = FALSE)

👉 NOTE: With variables such as no_food, we recoded the original question mainly for the sake of simplicity. This simplification can be useful as it reduces the number of parameters in our model. However, there may be distinct differences between each level that may produce different results.

If you find that your laptop is unable to handle the full data set without running slowly, try experimenting with the following code. This takes a random sample of the data, stratifying by country so the sampling algorithm doesn’t take more data from one country and less from another.

wvs = wvs.groupby("iso3c").sample(frac=0.25,random_state=123)Understanding life satisfaction: some exploratory data analysis (EDA) (5 minutes)

Here are a couple of graphs that tell a few stories about wvs.

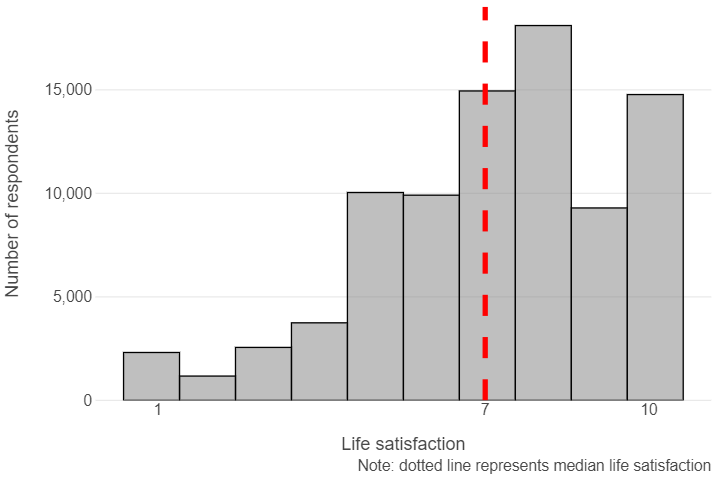

Median life satisfaction appears to be relatively high in the sample (7 out of 10)

med_satisfaction = np.median(wvs["satisfaction"])

(

ggplot(wvs, aes("satisfaction")) +

geom_histogram(fill = "grey", colour = "black", bins = 10, alpha = 0.5) +

geom_vline(xintercept = med_satisfaction, linetype = "dashed", size = 2, colour = "red") +

scale_x_continuous(breaks = [1, med_satisfaction, 10]) +

theme_minimal() +

theme(panel_grid_minor = element_blank(),

panel_grid_major_x=element_blank()) +

labs(x = "Life satisfaction", y = "Number of respondents",

caption = "Note: dotted line represents median life satisfaction")

)

Life satisfaction tracks positively with financial situation

wvs_count = wvs.value_counts(["financial_situ", "satisfaction"]).reset_index()

(

ggplot(wvs_count, aes("financial_situ", "satisfaction", size = "count")) +

geom_point() +

scale_x_continuous(breaks = np.arange(2, 12, 2)) +

scale_y_continuous(breaks = np.arange(2, 12, 2)) +

theme(panel_grid = element_blank(),

panel_background = element_rect(fill = "white"),

legend_position = "bottom") +

labs(x = "Financial situation", y = "Life satisfaction")

)

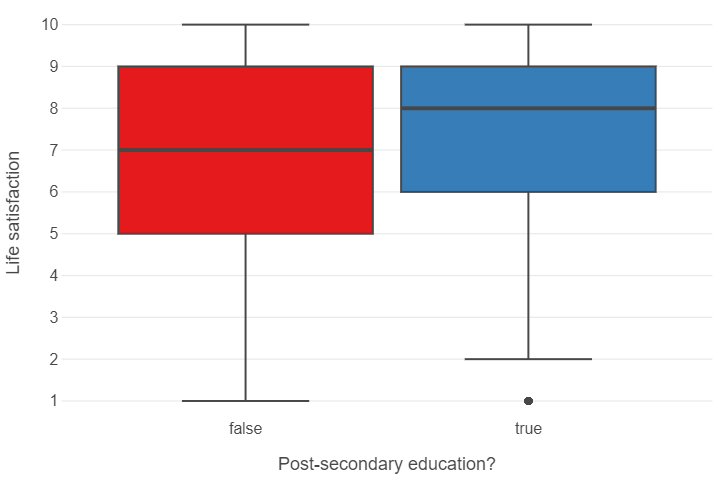

The median individual with post-secondary education has a higher life satisfaction than the median individual without

(

ggplot(wvs, aes("post_second_edu", "satisfaction", fill = "post_second_edu")) +

geom_boxplot() +

theme_minimal() +

theme(panel_grid_minor = element_blank(),

panel_grid_major_x = element_blank(),

legend_position="none") +

labs(x = "Post-secondary education?", y = "Life satisfaction")

)

Understanding life satisfaction: the hypothesis-testing approach (5 minutes)

Why do some people have a higher life satisfaction than others? This is one question that a quantitative social scientist might answer by exploring the magnitude and precision of a series of variables. Suppose we hypothesised that individuals with post-secondary level education have greater life satisfaction relative to those who do not. We can estimate a linear regression model by using satisfaction as the dependent variable and post_second_edu as the independent variable.

To estimate a linear regression with interpretable output in Python, we can use the sm.OLS function, which requires two things:

- One or more features plus a constant

- An outcome

Let’s do this now. We can print the summary method to get information on the coefficient estimate for post_second_edu.

# Convert post_second_edu to float

X = wvs["post_second_edu"].astype(float)

# Add a constant

X = sm.add_constant(X)

# Isolate the feature column

y = wvs["satisfaction"]

# Build an OLS and print its output

model_univ = sm.OLS(y,X).fit()

print(model_univ.summary())

OLS Regression Results

==============================================================================

Dep. Variable: satisfaction R-squared: 0.002

Model: OLS Adj. R-squared: 0.002

Method: Least Squares F-statistic: 42.24

Date: Thu, 30 Jan 2025 Prob (F-statistic): 8.23e-11

Time: 10:56:27 Log-Likelihood: -47959.

No. Observations: 21715 AIC: 9.592e+04

Df Residuals: 21713 BIC: 9.594e+04

Df Model: 1

Covariance Type: nonrobust

===================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------

const 7.0588 0.018 387.461 0.000 7.023 7.094

post_second_edu 0.2071 0.032 6.500 0.000 0.145 0.270

==============================================================================

Omnibus: 1373.715 Durbin-Watson: 1.793

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1650.277

Skew: -0.673 Prob(JB): 0.00

Kurtosis: 3.106 Cond. No. 2.41

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.We see that individuals with post-secondary education have a positive and statistically significant (p < 0.001) increase in life satisfaction of about 0.2 points.

👉 NOTE: The process of hypothesis testing is obviously more involved when using observational data than is portrayed by this simple example. Control variables will almost always be incorporated and, increasingly, identification strategies will be used to uncover causal effects. The end result, however, will involve as rigorous an attempt at falsifying a hypothesis as can be provided with the data.

For an example of how multivariate regression is used, we can run the following code.

# Create a function that normalises variables

def normalise(var):

return (var-var.mean())/var.std()

# Create a data frame of features

X = wvs.drop(["satisfaction","iso3c"],axis=1)

# Identify which features are floats, categories and booleians

X_float = X.filter(items=["age","financial_situ","relig_import"],axis=1)

X_cat = X.filter(items=["employment","better_living"],axis=1)

X_bool = X[X.columns[~X.columns.isin(X_float+X_cat)]]

# Normalise numeric features

X_float = X_float.apply(lambda x: normalise(x),axis=0)

# Get dummies from categorical features

X_cat = pd.get_dummies(X_cat,drop_first=True, dtype=int)

# Convert booleian features to integers

X_bool = X_bool.astype(int)

# Concatenate to final data frame

X = pd.concat([X_float,X_cat,X_bool],axis=1)

# Add a constant

X = sm.add_constant(X)

# ISOLATING OUR OUTCOME

y = wvs["satisfaction"]# BUILDING / SUMMARISING OUR MODEL

model_multiv = sm.OLS(y,X).fit()

print(model_multiv.summary())

OLS Regression Results

==============================================================================

Dep. Variable: satisfaction R-squared: 0.324

Model: OLS Adj. R-squared: 0.323

Method: Least Squares F-statistic: 472.3

Date: Thu, 30 Jan 2025 Prob (F-statistic): 0.00

Time: 10:56:34 Log-Likelihood: -43730.

No. Observations: 21715 AIC: 8.751e+04

Df Residuals: 21692 BIC: 8.769e+04

Df Model: 22

Covariance Type: nonrobust

=================================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------------------

const 7.1578 0.041 176.680 0.000 7.078 7.237

age 0.0019 0.016 0.118 0.906 -0.030 0.034

financial_situ 1.1439 0.013 85.712 0.000 1.118 1.170

relig_import 0.2020 0.013 15.168 0.000 0.176 0.228

employment_House wife/husband -0.0497 0.044 -1.129 0.259 -0.136 0.037

employment_Other 0.0397 0.114 0.348 0.728 -0.184 0.263

employment_Part time 0.1444 0.047 3.080 0.002 0.052 0.236

employment_Retired -0.0248 0.048 -0.514 0.608 -0.119 0.070

employment_Self employed 0.0224 0.040 0.563 0.573 -0.055 0.100

employment_Student -0.0373 0.061 -0.608 0.543 -0.158 0.083

employment_Unemployed -0.1534 0.050 -3.043 0.002 -0.252 -0.055

better_living_Better off 0.0211 0.029 0.727 0.467 -0.036 0.078

better_living_Worse off -0.4207 0.039 -10.845 0.000 -0.497 -0.345

social_trust 0.0517 0.030 1.720 0.085 -0.007 0.111

male -0.0582 0.027 -2.190 0.029 -0.110 -0.006

post_second_edu -0.0115 0.028 -0.411 0.681 -0.066 0.043

rural -0.0191 0.028 -0.692 0.489 -0.073 0.035

married 0.1937 0.028 6.980 0.000 0.139 0.248

no_food -0.2239 0.041 -5.414 0.000 -0.305 -0.143

no_safety -0.0114 0.036 -0.313 0.754 -0.083 0.060

no_medical -0.1025 0.037 -2.802 0.005 -0.174 -0.031

no_cash 0.0399 0.034 1.171 0.242 -0.027 0.107

no_shelter -0.2195 0.052 -4.204 0.000 -0.322 -0.117

==============================================================================

Omnibus: 873.122 Durbin-Watson: 1.887

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1990.498

Skew: -0.248 Prob(JB): 0.00

Kurtosis: 4.398 Cond. No. 15.1

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.Interestingly, we can see that the coefficient estimate for post_second_edu is now negative and significant, albeit at a lower level than before (p < 0.05).

👉 NOTE: p-values are useful to machine learning scientists as they indicate which variables may yield a significant increase in model performance. However, p-hacking where researchers manipulate data to find results that support their hypothesis make it hard to tell whether or not a relationship held up after honest attempts at falsification. This can range from using a specific modelling approach that produces statistically significant (while failing to report others that do not) findings to outright manipulation of the data. For a recent egregious case of the latter, we recommend the Data Falsificada series.

Predicting life satisfaction: the machine learning approach (30 minutes)

Machine learning scientists take a different approach. Our aim, in this context, is to build a model that can be used to accurately predict how happy a person is using a mixture of features and, for some models, hyperparameters (which we will address in Lab 5).

Thus, rather than attempting to falsify the effects of causes, we are more concerned about the fit of the model in the aggregate when applied to unforeseen data.

To achieve this, we do the following:

- Split the data into training and test sets

- Build a model using the training set

- Evaluate the model on the test set

Let’s look at each of these in turn.

Split the data into training and test sets

It is worth considering what a training and test set is and why we might split the data this way.

A training set is data that we use to build (or “train”) a model. In the case of multivariate linear regression, we are using the training data to estimate a series of coefficients. Here is a made-up multivariate linear model with three coefficients derived from (non-existent) data to illustrate things.

def sim_model_preds(x1,x2,x3):

y = 1.1*x1 + 2.2*x2 + 3.3*x3

return yA test set is data that the model has not yet seen. We then apply the model to this data set and use an evaluation metric to find out how accurate our predictions are. For example, suppose we had a new observation where x1 = 10, x2 = 20 and x3 = 30 and y = 150. We can use the above model to develop a prediction.

sim_model_preds(10,20,30)

154.0We get a prediction of 154 points!

We can also calculate the amount of error we make by calculating residuals (actual value - predicted value).

# Code here❓Question: How many points are we off by?

Why do we evaluate our models using different data? Because, as stated earlier, machine learning scientists care about the applicability of a model to unforeseen data. If we were to evaluate the model using the training data, we obviously cannot do this to begin with. Furthermore, we cannot ascertain whether the model we have built can generalise to other data sets or if the model has simply learned the idiosyncrasies of the data it was used to train on. We will discuss the concept of overfitting throughout this course.

We can use train_test_split in sklearn.model_selection to split the data into training and test sets.

X_train, X_test, y_train, y_test = train_test_split(X, y, random_state = 123)👉 NOTE: Our data are purely cross-sectional, so we can use this approach. However, when working with more complex data structures (e.g. time series cross sectional), different approaches to splitting the data will need to be used.

Build a model using the training set

We will now switch our focus from statsmodels to scikit-learn, the latter being Python’s most comprehensive and popular machine learning library.

Below, we will see how simple it is to run a model in this library. We have done all the data cleaning needed, so we can just get to it!

# Create a model instance of a linear regression

linear_model = LinearRegression()

# Fit this instance to the training set

linear_model.fit(X_train, y_train)Evaluate the model using the test set

Now that we have trained a model, we can then evaluate its performance on the test set. We will look at two evaluation metrics:

- R-squared: the proportion of variance in the outcome explained by the model.

- Root mean squared error (RMSE): the amount of error a typical observation parameterised as the units used in the initial measurement.

# Create predictions for the test set

linear_preds = linear_model.predict(X_test)

# Calculate performance metrics

r2 = r2_score(y_test, linear_preds)

rmse = root_mean_squared_error(y_test, linear_preds)

# Print results

print(np.round(r2, 2), np.round(rmse, 2))

0.33 1.83🗣️ CLASSROOM DISCUSSION:

How can we interpret these results?

We find that the model explains ~ 33% of the test set variance in life satisfaction. We also find that our model predictions are off by ~ 1.8 points.

Graphically exploring where we make errors

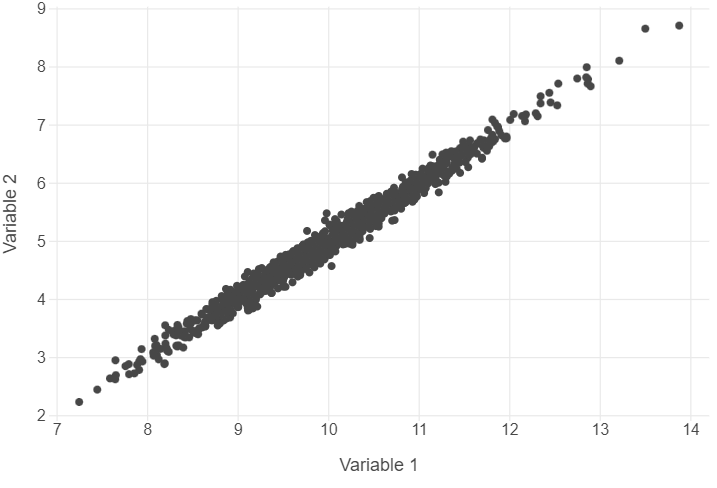

We are going to build some residual scatter plots which look at the relationship between the values fitted by the model for each observation and the residuals (actual - predicted values). Before we do this for our data, let’s take a look at an example where there is a near perfect relationship between two variables. As this very rarely exists in the social world, we will rely upon simulated data.

We translated and adapted this code from here.

# Set a seed for reproducibility

np.random.seed(123)

# Create the variance covariance matrix

sigma = [[1,0.99],[0.99,1]]

# Create the mean vector

mu = [10,5]

# Generate a multivariate normal distribution using 1,000 samples

v1, v2 = np.random.multivariate_normal(mu,sigma,1000).T

# Combine to a data frame

sim_data = pd.DataFrame({"V1":v1,"V2":v2})Plot the correlation

(

ggplot(sim_data, aes("V1", "V2")) +

geom_point() +

theme_minimal() +

theme(panel_grid_minor = element_blank()) +

labs(x = "Variable 1", y = "Variable 2")

)

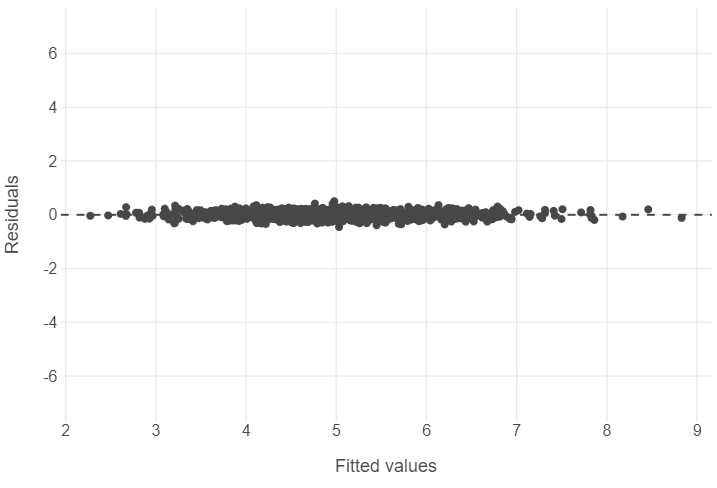

Residual plots

# Build a linear model

sim_fit = linear_model.fit(v1.reshape(-1,1),v2.reshape(-1,1))

sim_preds = linear_model.predict(v1.reshape(-1,1))

# Combine predictions / residuals to a data frame

sim_residuals_toplot = pd.DataFrame({"predictions": sim_preds.reshape(-1),

"residuals": v2 - sim_preds.reshape(-1)})

# Plot the results

(

ggplot(sim_residuals_toplot, aes("predictions", "residuals")) +

geom_hline(yintercept = 0, linetype = "dashed") +

geom_point() +

theme_minimal() +

theme(panel_grid_minor = element_blank()) +

scale_y_continuous(limits=[-7,7]) +

labs(x = "Fitted values", y = "Residuals")

)

Now let’s run this code for our model.

residuals_toplot = pd.DataFrame({"predictions": linear_preds,

"residuals": np.array(y_test) - linear_preds})

# Plot the output of residuals_toplot (x-axis = predictions, y-axis = residuals)🎯 ACTION POINTS why does the graph of the simulated data illustrate a more well-fitting model when compared to our actual data?

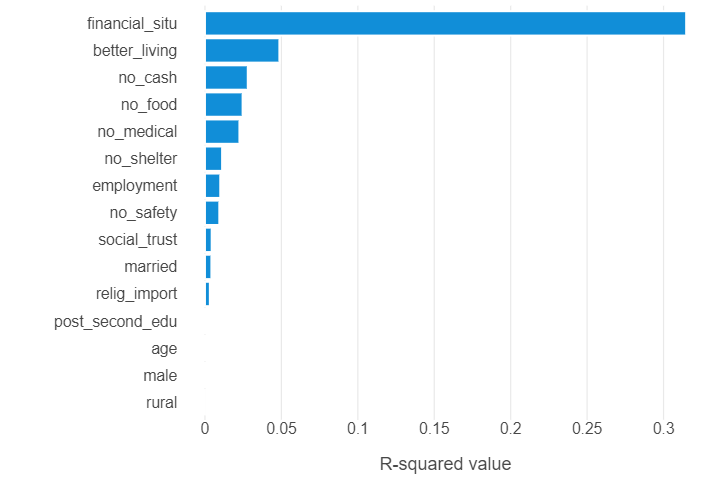

Introduction to using list comprehensions to aid feature selection (30 minutes)

👨🏻🏫 TEACHING MOMENT: Your tutor will take you through the code, so sit back, relax and enjoy!

Remember our univariate model earlier? We are going to do the same for all features so see which ones show the best improvements in predictive power.

We could build 15 different model objects, but this would be very inefficient. Instead, we are going to build a function that calculates the \(R2\) for a given feature and apply it to all features using a list comprehension.

Create a list of feature names

feature_names = wvs.drop(["iso3c","satisfaction"],axis=1).columnsDefine a function to get r-squared values for each feature

This gets a little tricky! Remember that we have transformed all our categorical features into one-hot encoded dummy variables. We need to therefore make sure that all dummies in one feature are included. The trick we’ve opted for is to use our original feature names to loop over. In the get_r2 we use a logical condition X_train.columns.str.contains(feature) which simply asks “does a given column name contain the string value of a given feature?”

def get_r2(feature):

"""

Runs a linear model using a subset of features in a training set and calculates

the r-squared for each model, using a test set. The output is a single value.

"""

# Create subsetted data

train = X_train[X_train.columns[X_train.columns.str.contains(feature)]]

test = X_test[X_test.columns[X_test.columns.str.contains(feature)]]

# Instantiate and run a linear model on subsetted data

linear_model = LinearRegression()

linear_model.fit(train,y_train)

# Create the predictions

preds = linear_model.predict(test)

# Calculate r-squared

r2 = r2_score(y_test,preds)

return r2We can check to see the function works by trying it on a feature or two. Let’s try this for financial situation.

financial_situ_r2 = get_r2("financial_situ")

print(np.round(financial_situ_r2, 2))

0.31Use a list comprehension to loop get_r2 over all features

r2s = [get_r2(feat) for feat in feature_names]Create a data frame showing the r-squared for each feature

linear_output = pd.DataFrame({"feature":feature_names,"r2":r2s})

linear_output = linear_output.sort_values(by = "r2")Plot the results!

(

ggplot(linear_output, aes("r2", "feature")) +

geom_bar(stat = "identity") +

theme_minimal() +

theme(panel_grid_minor = element_blank(),

panel_grid_major_y = element_blank()) +

labs(x = "R-squared value", y = "")

)

Using penalised linear regression to perform feature selection (20 minutes)

We are now going to experiment with a lasso regression which, in this case, is a linear regression that uses a so-called hyperparameter - a “dial” built into a given model that can be experimented with to improve model performance. The hyperparameter in this case is a regularisation penalty which takes the value of a non-negative number. This penalty can shrink the magnitude of coefficients down to zero and the larger the penalty, the more shrinkage occurs.

Step 1: Create a lasso model

Run the following code. This builds a lasso model with the penalty parameter set to 0.01.

lasso_model = Lasso(alpha = 0.01)

lasso_model.fit(X_train, y_train)Step 2: Extract lasso coefficients

# Create a data frame with feature columns and Lasso coefficients

lasso_output = pd.DataFrame({"feature": X_train.columns, "coefficient": lasso_model.coef_})

# Code a positive / negative vector

lasso_output["positive"] = np.where(lasso_output["coefficient"] >= 0, True, False)

# Take the absolute value of the coefficients

lasso_output["coefficient"] = np.abs(lasso_output["coefficient"])

# Remove the constant and sort the data frame by (absolute) coefficient magnitude

lasso_output = lasso_output.query("feature != 'const'").sort_values("coefficient")🎯 ACTION POINTS What is the output? Which coefficients have been shrunk to zero? What is the most important feature?

Step 3: Create a bar plot

# Code hereStep 4: Evaluate on the test set

Although a different model is used, the code for evaluating the model on the test set is exactly the same as earlier.

# Apply model to test set

# Calculate performance metrics

# Print rounded PMs🗣️ CLASSROOM DISCUSSION:

What feature is the largest positive / negative predictor of life satisfaction? Does this model represent an improvement on the linear model?

(Bonus) Step 5: Experiment with different penalties

This is your chance to try out different penalties. Can you find a penalty that improves test set performance?

# Instantiate a lasso model

# Fit the model to the training data

# Apply the model to the test set

# Calculate performance metrics

# Print the rounded metrics👉 NOTE: In labs 4 and 5, we are going to use a method called k-fold cross validation to systematically test different combinations of hyperparameters for models such as the lasso.