✅ A model solution for the W05 formative

What follows is a possible solution for the W05 formative.

Library import code

#| code-fold: true

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import plotly.express as px

import plotly.graph_objects as go

import numpy as np

import missingno as msno

import statsmodels.api as sm

from statsmodels.stats.outliers_influence import variance_inflation_factor

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression, Ridge, Lasso, ElasticNet

from sklearn.preprocessing import StandardScaler

from sklearn.experimental import enable_iterative_imputer

from sklearn.impute import IterativeImputer

from sklearn.ensemble import RandomForestRegressor

from sklearn.feature_selection import RFE

from sklearn.feature_selection import SequentialFeatureSelector

from sklearn.feature_selection import mutual_info_regression

from sklearn.metrics import (

mean_absolute_error,

mean_squared_error,

r2_score,

confusion_matrix,

classification_report,

accuracy_score,

precision_score,

recall_score,

f1_score

)Make sure to import all libraries at the top of your document.

This ensures that:

- All dependencies are declared transparently.

- Your code is reproducible from a clean session.

- Readers (and markers) can immediately see which packages are required.

- Execution does not depend on hidden state from previous notebook cells.

Avoid importing libraries midway through the document unless absolutely necessary. A clean, well-structured script or Quarto document should run from top to bottom without manual intervention.

Question 1 – Understanding the CEPII bilateral trade data

Before constructing any indicators, we must fully understand what this dataset represents and how it is structured. We do not jump into aggregation before understanding the economic meaning of a row.

Loading the dataset

We load the dataset in full.

gravity = pd.read_csv("../../data/Gravity_V202211.csv")

gravity.shape(4699296, 87)When loading data, make sure to use a relative path (and not an absolute path) that mirrors your repository structure.

Absolute paths (e.g. C:/Users/...) only work on your machine and break reproducibility.

Relative paths ensure that:

- The project runs on any machine.

- The repository structure is respected.

- Others can clone the repository and reproduce your results without editing file paths.

For example, if your repository structure is:

project/

│

├── data/

├── scripts/

└── analysis.qmdThen your data should be loaded using something like:

pd.read_csv("data/filename.csv")This makes the project portable and self-contained.

In this case, since the dataset is large and may exceed GitHub’s file size limit, it has not been pushed to the repository. In a fully reproducible project, explicit instructions would normally be provided explaining where to obtain the data and how to load it.

For example, a reproducible workflow would typically include:

- A link to the official data source (e.g. CEPII website).

- The exact dataset version used.

- Any preprocessing steps required before loading.

- Instructions on where to place the file within the repository structure (e.g.

data/raw/).

Without these details, another researcher cannot fully reproduce the analysis, even if all modelling code is provided.

When large datasets cannot be included directly, clear acquisition and setup instructions are essential for transparency and reproducibility.

The output tells us how many rows and columns the dataset contains: the number of rows is very large (close to 4.7 million rows), because each row represents a bilateral relationship (over many years of data collection).

We inspect the column names.

gravity.columnsIndex(['year', 'country_id_o', 'country_id_d', 'iso3_o', 'iso3_d', 'iso3num_o',

'iso3num_d', 'country_exists_o', 'country_exists_d',

'gmt_offset_2020_o', 'gmt_offset_2020_d', 'distw_harmonic',

'distw_arithmetic', 'distw_harmonic_jh', 'distw_arithmetic_jh', 'dist',

'main_city_source_o', 'main_city_source_d', 'distcap', 'contig',

'diplo_disagreement', 'scaled_sci_2021', 'comlang_off', 'comlang_ethno',

'comcol', 'col45', 'legal_old_o', 'legal_old_d', 'legal_new_o',

'legal_new_d', 'comleg_pretrans', 'comleg_posttrans',

'transition_legalchange', 'comrelig', 'heg_o', 'heg_d', 'col_dep_ever',

'col_dep', 'col_dep_end_year', 'col_dep_end_conflict', 'empire',

'sibling_ever', 'sibling', 'sever_year', 'sib_conflict', 'pop_o',

'pop_d', 'gdp_o', 'gdp_d', 'gdpcap_o', 'gdpcap_d', 'pop_source_o',

'pop_source_d', 'gdp_source_o', 'gdp_source_d', 'gdp_ppp_o',

'gdp_ppp_d', 'gdpcap_ppp_o', 'gdpcap_ppp_d', 'pop_pwt_o', 'pop_pwt_d',

'gdp_ppp_pwt_o', 'gdp_ppp_pwt_d', 'gatt_o', 'gatt_d', 'wto_o', 'wto_d',

'eu_o', 'eu_d', 'fta_wto', 'fta_wto_raw', 'rta_coverage', 'rta_type',

'entry_cost_o', 'entry_cost_d', 'entry_proc_o', 'entry_proc_d',

'entry_time_o', 'entry_time_d', 'entry_tp_o', 'entry_tp_d',

'tradeflow_comtrade_o', 'tradeflow_comtrade_d', 'tradeflow_baci',

'manuf_tradeflow_baci', 'tradeflow_imf_o', 'tradeflow_imf_d'],

dtype='object')We also inspect the first few rows.

gravity.head()| year | country_id_o | country_id_d | iso3_o | iso3_d | iso3num_o | iso3num_d | country_exists_o | country_exists_d | gmt_offset_2020_o | … | entry_time_o | entry_time_d | entry_tp_o | entry_tp_d | tradeflow_comtrade_o | tradeflow_comtrade_d | tradeflow_baci | manuf_tradeflow_baci | tradeflow_imf_o | tradeflow_imf_d | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1948 | ABW | ABW | ABW | ABW | 533.0 | 533.0 | 0 | 0 | NaN | … | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1 | 1949 | ABW | ABW | ABW | ABW | 533.0 | 533.0 | 0 | 0 | NaN | … | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2 | 1950 | ABW | ABW | ABW | ABW | 533.0 | 533.0 | 0 | 0 | NaN | … | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 3 | 1951 | ABW | ABW | ABW | ABW | 533.0 | 533.0 | 0 | 0 | NaN | … | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 4 | 1952 | ABW | ABW | ABW | ABW | 533.0 | 533.0 | 0 | 0 | NaN | … | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

5 rows × 87 columns

From this inspection, we identify:

iso3_o: exporting country (origin)iso3_d: importing country (destination)year: year of observationtradeflow_baci: value of exports (in USD)

What does one row represent?

Each row represents:

Exports from country A to country B in year t.

That means:

- The dataset is not country-level.

- The unit of observation is exporter–importer–year.

- Each exporting country appears multiple times per year (once per partner).

For example, if France exports to 150 countries in 2019, France will appear in 150 separate rows for that year.

This is why the dataset is described as bilateral rather than country-level.

Time coverage

We now inspect the time dimension.

years = gravity["year"].astype(int)

min_year = int(years.min())

max_year = int(years.max())

print(f"Start year: {min_year}, End year: {max_year}")Start year: 1948, End year: 2021This gives us the range of years present in the data i.e data that starts in 1948 and ends in 2021.

Let’s check whether all years in that range are present in the data or if there is any coverage gap:

expected_years = set(range(min_year, max_year + 1))

observed_years = set(years.unique())

missing_years = sorted(expected_years - observed_years)

if missing_years:

print("Missing years:", missing_years)

else:

print("No gaps in year coverage.")No gaps in year coverage.This means there is no gap in coverage within the range of years present in the dataset (i.e there is data for every year between 1948 and 2021)

Now, let’s check how many exporters are present per year.

exporters_per_year = (

gravity.groupby("year")["iso3_o"]

.nunique()

.reset_index(name="num_exporters")

)

fig = px.line(

exporters_per_year,

x="year",

y="num_exporters",

markers=True,

title="The number of exporting countries<br>stays constant over time",

)

fig.update_layout(

xaxis_title="Year",

yaxis_title="Number of exporters",

hovermode="x unified"

)

figThe number of exporters represented in the data stays constant over the year.

We also count the number of exporter–importer pairs per year.

pairs_per_year = gravity.groupby("year").size().reset_index(name="num_pairs")

fig = px.line(

pairs_per_year,

x="year",

y="num_pairs",

markers=True,

title="The number of exporter-importer pairs<br>is constant over time",

)

fig.update_layout(

xaxis_title="Year",

yaxis_title="Number of exporter-importer pairs",

hovermode="x unified"

)

figThe number of exporter-importer pairs is also constant over time. This only tells us that the data coverage is constant but doesn’t tell us much about trade patterns themselves

However, when we restrict attention to positive trade relationships — that is, exporter–importer pairs with strictly positive trade flows — a different picture emerges.

Unlike the total number of possible pairs, which is mechanically determined by the number of countries in the dataset, the number of active trade links reflects the extent to which countries are actually engaged in trade with one another.

positive_pairs = (

gravity[gravity["tradeflow_baci"] > 0]

.groupby("year")

.size()

.reset_index(name="positive_pairs")

)

fig = px.line(

positive_pairs,

x="year",

y="positive_pairs",

markers=True,

title="Increasing number of active trade relationships<br> suggests expanding global connectivity",

)

fig.update_layout(

xaxis_title="Year",

yaxis_title="Number of positive trade relationships pairs",

hovermode="x unified"

)

figThe plot of positive trade relationships shows a clear upward trend from the mid-1990s through the late 2010s. This suggests that over time, a larger number of country pairs are trading with one another. In other words, the global trade network becomes progressively more interconnected. The visible decline in 2020 is likely consistent with the disruption of global trade during the COVID-19 pandemic.

To better interpret this evolution, we compute network density, defined as the share of all possible exporter–importer pairs that exhibit positive trade:

\[ \text{Density} = \frac{\text{Number of positive trade relationships}}{\text{Total possible country pairs}} \]

This normalised measure accounts for the fact that the country set remains constant.

total_pairs = gravity.groupby("year").size()

positive_pairs = gravity[gravity["tradeflow_baci"] > 0].groupby("year").size()

density = (positive_pairs / total_pairs).reset_index(name="density")

fig = px.line(

density,

x="year",

y="density",

markers=True,

title="Increasing trade network density suggests<br> broader partner diversification at the global level",

)

fig.update_layout(

xaxis_title="Year",

yaxis_title="Network density",

hovermode="x unified"

)

figThe density plot reveals that the proportion of active trade relationships increases substantially over time — from roughly one-fifth of possible country pairs in the late 1990s to around one-half by the late 2010s.

This indicates not merely growth in trade volumes, but a structural deepening of global economic integration: countries are trading with a wider set of partners. The decline observed in 2020 again reflects a contraction in the effective connectivity of the global trade network.

Importantly, these patterns describe the structure of trade relationships, not the size of trade flows. They motivate the later construction of country-level concentration measures, since increasing network density does not necessarily imply that individual countries are diversified in their export portfolios.

Scale and skewness of bilateral trade flows

We begin by examining the distribution of bilateral trade values.

gravity["tradeflow_baci"].describe()count 6.948280e+05

mean 4.445421e+05

std 4.678032e+06

min 1.000000e-03

25% 6.392825e+01

50% 1.613026e+03

75% 3.154437e+04

max 5.009282e+08

Name: tradeflow_baci, dtype: float64The summary statistics reveal extreme right-skewness. The mean trade flow (≈ 444,542 USD) is almost 275 times larger than the median (≈ 1,613 USD), indicating that a small number of very large trade relationships dominate the average. In other words, the mean is not representative of a “typical” bilateral relationship.

Dispersion is also substantial. The standard deviation (≈ 4.7 million USD) exceeds the mean by roughly an order of magnitude, confirming heavy tails and large variability across country pairs.

The range is enormous: trade flows vary from 0.001 USD to over 500 million USD — spanning more than eleven orders of magnitude. This level of heterogeneity is characteristic of international trade data.

To better understand the lower tail of the distribution, we examine the proportion of very small trade flows:

float((gravity["tradeflow_baci"] < 100).mean())0.04170922623303576Approximately 4.2% of bilateral relationships involve trade flows below 100 USD. While not the majority, this confirms the presence of many economically negligible flows.

At the upper tail, the 99th percentile of trade flows is:

float(gravity["tradeflow_baci"].quantile(0.99))8171109.259739949Only 1% of trade relationships exceed roughly 8.17 million USD. Yet these large flows account for a disproportionately large share of global trade:

threshold = gravity["tradeflow_baci"].quantile(0.99)

top_1 = gravity[gravity["tradeflow_baci"] >= threshold]["tradeflow_baci"].sum()

total = gravity["tradeflow_baci"].sum()

float(top_1 / total)0.6258628801133919The top 1% of trade relationships account for approximately 62.6% of total trade value. This concentration highlights the dominance of major trading corridors (e.g. large economies trading with each other) in shaping global trade aggregates.

We also verify whether zero trade flows are present:

float((gravity["tradeflow_baci"] == 0).sum())0.0There are no exact zeros in this dataset; even very small flows are recorded as positive values. This is important for modelling decisions (e.g. log transformations), since we do not need to handle structural zeros explicitly.

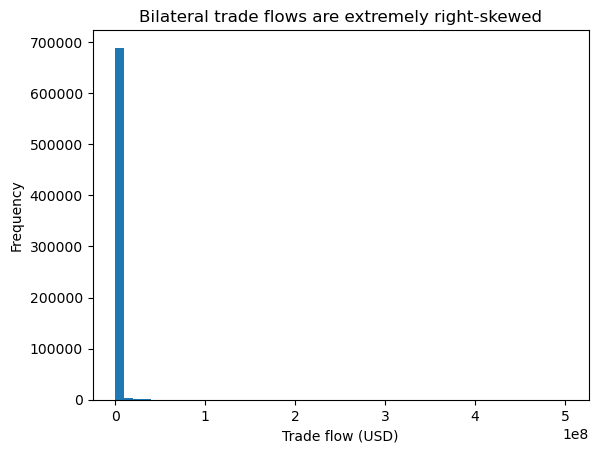

We now visualise the raw distribution.

plt.hist(gravity["tradeflow_baci"], bins=50)

plt.title("Bilateral trade flows are extremely right-skewed")

plt.xlabel("Trade flow (USD)")

plt.ylabel("Frequency")

plt.show()

The raw scale is dominated by a handful of very large trade flows, compressing the vast majority of observations near zero. This makes it difficult to visually interpret the structure of the bulk of the distribution.

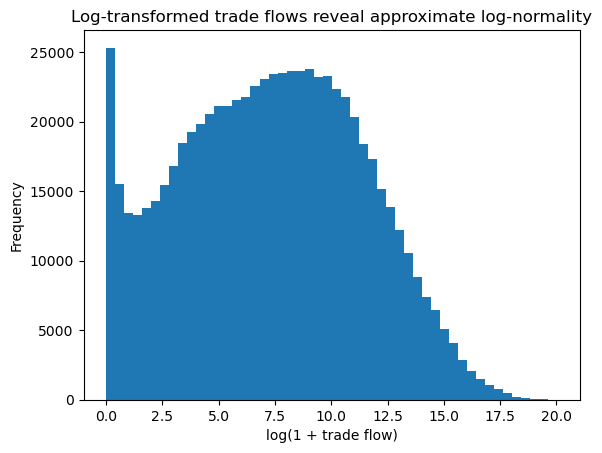

To better visualise dispersion across orders of magnitude, we examine log-transformed values.

plt.hist(np.log1p(gravity["tradeflow_baci"]), bins=50)

plt.title("Log-transformed trade flows reveal approximate log-normality")

plt.xlabel("log(1 + trade flow)")

plt.ylabel("Frequency")

plt.show()

After log transformation, the distribution becomes much more symmetric and approximately bell-shaped. This is consistent with well-established findings in gravity modelling, where trade flows are often assumed to follow a log-normal distribution.

These patterns have direct implications for later analysis:

- Raw trade values are unsuitable for linear modelling without transformation.

- Extreme skewness implies that large trade flows exert disproportionate influence.

- Concentration measures (e.g. HHI) may be heavily affected by dominant partners.

- Log transformations or normalised indicators are more appropriate summaries when constructing country-level variables.

In short, bilateral trade is highly unequal across country pairs: a small number of relationships account for the majority of global trade, while many relationships remain economically minor. This structural heterogeneity motivates careful aggregation and transformation before proceeding to country-level modelling.

Country-level illustration

To make the structure of bilateral trade relationships concrete, we focus on a single year and compare one large exporter to one smaller (but economically meaningful) exporter.

Before selecting a year, we reflect on what we want this illustration to capture. The earlier network density plots showed that global trade relationships expanded steadily through the 2000s and 2010s before contracting in 2020. Because 2020 reflects a major global disruption associated with the COVID-19 pandemic, using it for structural illustration risks capturing temporary shock effects rather than stable trade patterns.

We therefore select 2019 for illustration. This choice is motivated by three considerations:

- It is the most recent year prior to the pandemic shock, and therefore reflects relatively stable pre-disruption trade patterns.

- It lies near the peak of network density, meaning that the global trade network is highly interconnected.

- It maximises contemporary relevance while avoiding structural breaks.

gravity_2019 = gravity[gravity["year"] == 2019].copy()We first compute total exports by exporter in 2019.

totals_2019 = (

gravity_2019.groupby("iso3_o")["tradeflow_baci"]

.sum()

.sort_values(ascending=False)

)

totals_2019.head()iso3_o

CHN 2.602804e+09

USA 1.517438e+09

DEU 1.423811e+09

JPN 6.907045e+08

KOR 5.559240e+08

Name: tradeflow_baci, dtype: float64The upper tail of this distribution confirms what we expect: a small number of countries dominate global export volumes.

However, before selecting a “small exporter” for comparison, it is important to inspect the lower tail of the distribution carefully.

totals_2019.tail(15)iso3_o

VDR 0.0

CSK 0.0

VAT 0.0

MTQ 0.0

MYT 0.0

GUF 0.0

GLP 0.0

FRO 0.0

PRI 0.0

ESH 0.0

REU 0.0

DDR 0.0

SUN 0.0

LIE 0.0

SCG 0.0

Name: tradeflow_baci, dtype: float64Inspection of the bottom entries reveals that several codes have zero recorded exports in 2019. These include historical country codes (e.g. former political entities) and certain territorial or special-status entities that are not economically active exporters in this year.

Selecting the absolute smallest exporter mechanically would therefore produce a misleading comparison: we might end up comparing China to a historical code or a territory with no economic relevance.

To ensure that we select a country that meaningfully participates in trade in 2019, we restrict attention to exporters with strictly positive total exports.

positive_totals_2019 = totals_2019[totals_2019 > 0]

positive_totals_2019.tail(15)iso3_o

SHN 23101.794

STP 22278.950

TKL 19614.029

SXM 19429.307

TUV 17931.291

CXR 17878.056

TON 14860.064

TCA 14259.457

SPM 7418.826

MSR 6350.075

CCK 4618.688

MNP 3885.540

NFK 2756.989

WLF 1989.099

PCN 1922.017

Name: tradeflow_baci, dtype: float64This filtered list still contains very small entities. Among the smallest positive exporters, many correspond to micro-territories (e.g. Pitcairn Islands, Christmas Island, etc.), whose trade volumes are extremely small and whose economic structure differs fundamentally from that of sovereign states.

For an analytically meaningful comparison, we therefore select:

CHN(China), the largest exporter in 2019, andTON(Tonga), a small sovereign exporter from the lower tail of the positive-export distribution.

This allows us to compare:

- A globally dominant trading economy,

- A small island economy that actively participates in international trade.

large_country = "CHN"

small_country = "TON"

positive_totals_2019.loc[[large_country, small_country]]iso3_o

CHN 2.602804e+09

TON 1.486006e+04

Name: tradeflow_baci, dtype: float64The scale difference is enormous. China’s total exports are approximately:

\[ \frac{2.60 \times 10^9}{1.49 \times 10^4} \approx 175{,}000 \]

times larger than Tonga’s.

This illustrates the extreme dispersion in global export capacity across countries. However, scale alone does not capture how exports are distributed across partners.

We therefore examine export concentration through the share of exports accounted for by the top five destinations.

We compute the share of exports accounted for by the top five destinations for each country.

def top_k_share(df_country, k=5):

total = df_country["tradeflow_baci"].sum()

top_k = df_country.sort_values("tradeflow_baci", ascending=False).head(k)

share = top_k["tradeflow_baci"].sum() / total

return share, top_k

chn_data = gravity_2019[gravity_2019["iso3_o"] == large_country]

ton_data = gravity_2019[gravity_2019["iso3_o"] == small_country]

chn_top5_share, chn_top5 = top_k_share(chn_data, k=5)

ton_top5_share, ton_top5 = top_k_share(ton_data, k=5)

print(f"Top-5 export share for {large_country}: {chn_top5_share:.3f}")

print(f"Top-5 export share for {small_country}: {ton_top5_share:.3f}")Top-5 export share for CHN: 0.402

Top-5 export share for TON: 0.897We also inspect the identities and trade values of the top partners.

chn_top5[["iso3_d", "tradeflow_baci"]]| iso3_d | tradeflow_baci | |

|---|---|---|

| 763233 | USA | 4.270040e+08 |

| 753095 | HKG | 2.620376e+08 |

| 754353 | JPN | 1.495683e+08 |

| 754871 | KOR | 1.109780e+08 |

| 750357 | DEU | 9.674598e+07 |

ton_top5[["iso3_d", "tradeflow_baci"]]| iso3_d | tradeflow_baci | |

|---|---|---|

| 4175817 | USA | 5596.096 |

| 4167455 | KOR | 2648.902 |

| 4159537 | AUS | 2127.026 |

| 4171007 | NZL | 1993.041 |

| 4166937 | JPN | 969.765 |

This difference is economically meaningful.

For China:

- The top five destinations (USA, HKG, JPN, KOR, DEU) account for about 40% of total exports.

- Exports are spread across many partners.

- Even the largest bilateral flow (to the USA) represents only a fraction of total exports.

For Tonga:

- The top five destinations account for nearly 90% of total exports.

- Trade is highly concentrated.

- A small number of relationships dominate total exports.

- The largest bilateral flow (to the USA) represents a substantial share of Tonga’s total exports.

This contrast illustrates two structurally different trade profiles:

| Large diversified exporter (China) | Small concentrated exporter (Tonga) |

|---|---|

| High total exports | Very low total exports |

| Many trading partners | Fewer economically meaningful partners |

| Lower top-5 share | Very high top-5 share |

| More diversified export structure | High partner dependence |

The key takeaway is that countries differ not only in how much they trade, but in how concentrated their trade relationships are.

This matters for development and welfare because:

- High concentration can increase vulnerability to partner-specific shocks.

- Diversification may reduce exposure to geopolitical or demand risk.

- Concentration patterns may correlate with institutional development, income level, or trade policy structure.

However, our comparison so far is descriptive and country-specific.

To move from anecdotal comparison to systematic analysis, we require formal country-level measures of concentration and diversification that:

- Apply consistently to all exporters,

- Collapse bilateral flows into one interpretable summary per country,

- Can be merged with macroeconomic outcomes.

Why aggregation is required

The country-level illustration above makes a deeper structural issue explicit.

Each row in the CEPII dataset represents:

- One exporter,

- One importer,

- One year,

- One bilateral trade flow value.

For China in 2019, there are hundreds of rows — one for each trading partner. For Tonga, there are also hundreds of rows — even though many flows are extremely small.

In other words, the CEPII dataset is structured at the exporter–importer–year level.

However, our outcome variable — adjusted net national income growth — is measured at the country-year level.

This creates a fundamental mismatch in the unit of analysis.

If we attempted to regress country-level income growth directly on bilateral trade flows:

- Each country would appear hundreds of times in the regression dataset.

- Observations would not be independent at the country level.

- Countries with more trading partners would mechanically receive more weight.

- Countries would effectively be double-counted (or counted hundreds of times).

- The unit of analysis would be inconsistent between predictors and outcome.

This would invalidate interpretation and distort inference.

The problem is not merely technical — it is conceptual. We would be combining:

- A country-level outcome,

- With relationship-level predictors.

These operate at different levels of aggregation.

To build a coherent modelling dataset, we must therefore align the unit of analysis.

Aggregation is necessary in order to:

- Align the unit of analysis to country-year,

- Prevent double-counting,

- Ensure that each country contributes one observation per year,

- Construct interpretable summaries of trade structure.

Importantly, aggregation is not a neutral transformation.

The moment we aggregate bilateral flows, we must decide which aspect of trade structure we wish to emphasise:

- Total export scale?

- Concentration across partners?

- Diversification?

- Dependence on a single dominant partner?

- Exposure to geopolitical clustering?

Each aggregation choice encodes an economic assumption about what matters.

The China–Tonga comparison illustrates why this matters. China trades with many partners and spreads risk across them, while Tonga relies heavily on a small number of destinations. A country-level measure should capture such structural differences systematically rather than anecdotally.

Thus, aggregation fundamentally shifts the level of analysis:

- From individual trade relationships,

- To structural characteristics of a country’s overall trade profile.

In the next question, we formalise this step by constructing country-level concentration indicators — such as the Herfindahl–Hirschman Index (HHI) — which summarise how export shares are distributed across trading partners.

This transforms bilateral data into a modelling-ready country-level dataset while preserving economically meaningful information about trade structure.

Question 2 – Aggregating bilateral trade flows into country-level indicators

In Question 1, we established that the CEPII Gravity dataset is structured at the exporter–importer–year level, while our outcome variable (adjusted net national income growth) is measured at the country level. To align the unit of analysis, we must aggregate bilateral flows into country-level indicators.

In this question, we construct interpretable measures of export structure for each exporting country in a given year. We continue using 2019, consistent with Question 1.

gravity_2019 = gravity[gravity["year"] == 2019].copy()Missingness and what we do about it (before aggregation)

Before constructing concentration indicators, we must check whether bilateral trade flows are fully observed.

gravity_2019[["iso3_o", "iso3_d", "tradeflow_baci"]].isna().sum()iso3_o 0

iso3_d 0

tradeflow_baci 32384

dtype: int64In our data:

- exporter (

iso3_o): no missing values - importer (

iso3_d): no missing values - trade flow (

tradeflow_baci): non-trivial missingness

We also verify whether zeros are used to represent “no trade”:

int((gravity_2019["tradeflow_baci"] == 0).sum())0There are no zero trade flows in 2019. This matters because it implies that missing trade values are not being explicitly coded as zeros.

At this stage, we must make a principled decision: how should missing trade flows be treated when constructing a country-level concentration measure?

A tempting option would be to impute missing flows. However, imputation here would be problematic for two reasons:

- Trade flows are extremely skewed, and missingness is unlikely to be random. Model-based imputation would add strong assumptions about the bilateral trade-generating process.

- Our goal is not to predict missing bilateral trade flows. Our goal is to construct a transparent structural summary of trade relationships. If we impute flows, the resulting HHI would become partly model-driven rather than purely data-derived.

Given this, the most defensible approach is to compute concentration indices conditional on observed trade flows. That is, we drop missing tradeflow values and interpret them as unobserved or negligible flows for the purpose of measuring recorded trade concentration.

We proceed by restricting to observed flows:

gravity_2019_obs = gravity_2019.dropna(subset=["tradeflow_baci"]).copy()

gravity_2019_obs[["iso3_o", "iso3_d", "tradeflow_baci"]].isna().sum()iso3_o 0

iso3_d 0

tradeflow_baci 0

dtype: int64This choice should be kept in mind when interpreting HHI later: concentration is computed over recorded bilateral flows, and countries with poorer coverage may have concentration measures that reflect data limitations as well as genuine trade structure.

Step 1: Total exports by exporter (from observed flows)

We compute total exports for each exporter as the sum of its observed bilateral flows:

total_exports_2019 = (

gravity_2019_obs

.groupby("iso3_o")["tradeflow_baci"]

.sum()

.rename("total_exports")

)

total_exports_2019.head()iso3_o

ABW 9.372390e+04

AFG 2.496945e+06

AGO 3.686795e+07

AIA 4.718417e+04

ALB 2.830572e+06

Name: total_exports, dtype: float64Export shares will require dividing by total exports, so we verify that totals are strictly positive:

int((total_exports_2019 <= 0).sum())0Any exporter with total exports equal to zero would yield undefined shares. (In 2019, exporters with zero total exports were already identified in Question 1; working with observed flows ensures that HHI is only defined for exporters with positive total exports.)

Step 3: Export concentration (HHI)

We compute the Herfindahl–Hirschman Index:

\[ HHI_c = \sum_j s_{cj}^2 \]

Intuition:

- If exports are spread evenly across many partners → shares are small → HHI is low.

- If exports are concentrated in a few partners → some shares are large → HHI is high.

- If all exports go to one partner → HHI = 1.

hhi_2019 = (

gravity_2019_obs

.groupby("iso3_o")["export_share"]

.apply(lambda x: (x**2).sum())

.rename("hhi")

)

hhi_2019.head()iso3_o

ABW 0.271831

AFG 0.284480

AGO 0.359164

AIA 0.363542

ALB 0.212542

Name: hhi, dtype: float64We combine total exports and HHI into a clean country-level dataset:

trade_structure_2019 = pd.concat([total_exports_2019, hhi_2019], axis=1)

trade_structure_2019.head()| total_exports | hhi | |

|---|---|---|

| iso3_o | ||

| ABW | 9.372390e+04 | 0.271831 |

| AFG | 2.496945e+06 | 0.284480 |

| AGO | 3.686795e+07 | 0.359164 |

| AIA | 4.718417e+04 | 0.363542 |

| ALB | 2.830572e+06 | 0.212542 |

Each row now corresponds to one exporter in 2019, which is the correct level of analysis for merging with macro-level indicators.

Alternative interpretations of concentration

The Herfindahl–Hirschman Index (HHI) measures export concentration as

\[ HHI_c = \sum_j s_{cj}^2 \]

where \(s_{cj}\) is the share of exports from country \(c\) going to partner \(j\).

Because shares are squared:

- Large export shares are amplified.

- Small shares contribute very little.

- Concentration increases nonlinearly as exports become dependent on a few destinations.

Although HHI is widely used, its raw values are not always intuitive. For example, what does an HHI of 0.19 or 0.36 mean economically?

To make interpretation clearer, it is common to report simple transformations.

Diversification index: \(1 - HHI\)

\[ \text{Diversification}_c = 1 - HHI_c \]

This simply reverses the scale:

- High HHI → low diversification

- Low HHI → high diversification

It remains bounded between 0 and 1 and preserves the same ranking across countries.

Effective number of partners: \(\frac{1}{HHI}\)

\[ \text{Effective partners}_c = \frac{1}{HHI_c} \]

This transformation is especially intuitive.

If exports were evenly distributed across ( k ) partners, then

\[ HHI = \frac{1}{k} \quad \Rightarrow \quad \frac{1}{HHI} = k \]

Thus, \(1/HHI\) approximates the number of equally weighted partners that would produce the observed concentration level.

For illustration:

- If HHI = 0.50 → effective partners ≈ 2

- If HHI = 0.20 → effective partners ≈ 5

- If HHI = 0.10 → effective partners ≈ 10

Using our actual summary statistics:

- Mean HHI ≈ 0.192

- Median HHI ≈ 0.133

- Minimum ≈ 0.031

- Maximum ≈ 0.849

This implies:

- The average country’s trade structure resembles being evenly spread across roughly 5 effective partners.

- Some countries are highly diversified (HHI ≈ 0.03 → ≈ 32 effective partners).

- Some are extremely concentrated (HHI ≈ 0.85 → ≈ 1.2 effective partners).

We compute these transformations below:

trade_structure_2019["diversification"] = 1 - trade_structure_2019["hhi"]

trade_structure_2019["effective_partners"] = 1 / trade_structure_2019["hhi"]

trade_structure_2019.head()| total_exports | hhi | diversification | effective_partners | |

|---|---|---|---|---|

| iso3_o | ||||

| ABW | 9.372390e+04 | 0.271831 | 0.728169 | 3.678754 |

| AFG | 2.496945e+06 | 0.284480 | 0.715520 | 3.515187 |

| AGO | 3.686795e+07 | 0.359164 | 0.640836 | 2.784246 |

| AIA | 4.718417e+04 | 0.363542 | 0.636458 | 2.750712 |

| ALB | 2.830572e+06 | 0.212542 | 0.787458 | 4.704949 |

These transformations do not add new information; they provide more interpretable representations of the same concentration structure.

Coverage diagnostic (important given missingness)

Because tradeflow_baci contains missing values, it is important to assess whether measured export concentration may partly reflect incomplete bilateral coverage.

We compute, for each exporter, the fraction of potential bilateral observations in 2019 that have missing tradeflow values:

coverage_2019 = (

gravity_2019

.assign(missing_flow=gravity_2019["tradeflow_baci"].isna())

.groupby("iso3_o")["missing_flow"]

.mean()

.rename("missing_flow_rate")

)

trade_structure_2019 = trade_structure_2019.merge(

coverage_2019,

left_index=True,

right_index=True,

how="left"

)

trade_structure_2019[["hhi", "missing_flow_rate"]].describe()| hhi | missing_flow_rate | |

|---|---|---|

| count | 224.000000 | 224.000000 |

| mean | 0.191896 | 0.460867 |

| std | 0.166603 | 0.209810 |

| min | 0.031245 | 0.115079 |

| 25% | 0.080940 | 0.285714 |

| 50% | 0.133119 | 0.466270 |

| 75% | 0.223843 | 0.627976 |

| max | 0.849354 | 0.924603 |

From the summary statistics:

- Mean missing_flow_rate ≈ 0.461

- Median ≈ 0.466

- Some exporters exceed 0.90

This means that, on average, nearly half of potential bilateral partner observations are missing in 2019.

However, missing_flow_rate measures the fraction of partner pairs without recorded tradeflow, not the fraction of trade value missing.

Given the extreme skewness documented in Question 1:

- Trade value is concentrated in relatively few large bilateral relationships.

- Many missing entries likely correspond to very small or negligible flows.

- HHI is driven primarily by large shares.

Nonetheless, missingness could mechanically increase measured concentration if:

- Many small flows are unrecorded,

- Only dominant relationships are recorded,

- Smaller economies have poorer reporting coverage.

For this reason:

- HHI should be interpreted as concentration conditional on recorded flows.

- The coverage diagnostic allows later robustness checks.

- We retain missing_flow_rate for interpretation and possible modelling controls.

Importantly, we deliberately chose not to impute missing bilateral flows. Imputation would introduce model-driven structure into HHI, potentially biasing concentration downward by adding artificial small flows. Instead, we preserve transparency and compute concentration strictly from observed data.

Why these indicators are meaningful

Total exports measure scale.

Concentration measures capture structure.

These dimensions are conceptually distinct.

Two countries can:

- Have similar export totals,

- Yet differ dramatically in partner dependence.

A concentrated exporter:

- Is more exposed to partner-specific demand shocks,

- May be vulnerable to trade disruptions,

- May reflect limited diversification or geopolitical dependence.

A diversified exporter:

- Spreads exposure across many markets,

- May be more resilient,

- May reflect broader integration or more complex export baskets.

Because HHI is scale-invariant, it captures structural features independently of country size. It therefore complements total trade measures rather than duplicating them.

These structural characteristics are plausible candidates for explaining—or at least correlating with—welfare-relevant outcomes such as adjusted net national income growth.

Resulting dataset

After aggregation, we obtain a country-level dataset for 2019 containing:

- Total exports (scale)

- HHI (concentration)

- Diversification measures

- Effective number of partners

- Missing-flow coverage diagnostic

trade_structure_2019.reset_index().head()| iso3_o | total_exports | hhi | diversification | effective_partners | missing_flow_rate | |

|---|---|---|---|---|---|---|

| 0 | ABW | 9.372390e+04 | 0.271831 | 0.728169 | 3.678754 | 0.690476 |

| 1 | AFG | 2.496945e+06 | 0.284480 | 0.715520 | 3.515187 | 0.464286 |

| 2 | AGO | 3.686795e+07 | 0.359164 | 0.640836 | 2.784246 | 0.400794 |

| 3 | AIA | 4.718417e+04 | 0.363542 | 0.636458 | 2.750712 | 0.710317 |

| 4 | ALB | 2.830572e+06 | 0.212542 | 0.787458 | 4.704949 | 0.476190 |

Each row now corresponds to one exporting country, fully aligned with the unit of the outcome variable. The dataset is therefore ready to be merged with World Bank and KOF indicators in Question 3.

Question 3 – Building the Modelling Dataset

In Questions 1 and 2, we explored the CEPII Gravity dataset and constructed country-level trade structure indicators using 2019 as a worked example. However, the final modelling dataset must satisfy several structural requirements.

A coherent modelling dataset must ensure:

- Trade predictors and the outcome variable refer to the same year.

- The modelling year is selected transparently and empirically.

- The outcome variable is fully observed in the modelling sample.

- Predictor missingness is handled explicitly and appropriately.

- Any preprocessing decisions avoid information leakage into later modelling steps.

In this question, we determine the modelling year, recompute trade structure indicators for that year, merge all datasets, and diagnose missingness. We deliberately do not perform imputation here. That will be done in Question 4 after the training/test split to avoid leakage.

3.1 Choosing a common year

The core issue here is temporal alignment. We cannot build a meaningful predictive model if predictors and outcome refer to different years, because the model would then implicitly combine multiple “states of the world” without acknowledging lags, shocks, or timing assumptions. For example, a country’s trade structure in 2018 and its adjusted net national income growth in 2020 are not comparable without explicitly modelling the lag and its economic interpretation. Even if the model “runs”, the coefficients and performance would not correspond to a coherent economic story.

So the goal of 3.1 is to identify a single year that is simultaneously valid for:

- CEPII-derived trade indicators (from Gravity),

- KOF Trade Globalisation indicators (de facto and de jure), and

- World Bank indicators (including the outcome).

We choose the year using an empirical criterion: maximise country overlap, while also ensuring the outcome is observed and the year is substantively interpretable (e.g., not dominated by structural shock regimes like COVID years unless that is explicitly part of the modelling goal).

3.1.1 Loading macroeconomic and globalisation datasets (and harmonising identifiers)

We load the World Bank and KOF datasets:

world_bank = pd.read_csv("../../data/world_bank_indicators_2017_2021.csv")

kof = pd.read_excel("../../data/kof_trade_globalisation.xlsx")Before doing anything else, we inspect the structure, because different sources often use different country identifiers and variable naming conventions.

print("World Bank dataset columns:", world_bank.columns)

print("KOF dataset columns:", kof.columns)World Bank dataset columns: Index(['country_code', 'country_name', 'year', 'NY.GDP.TOTL.RT.ZS',

'NY.ADJ.NNAT.GN.ZS', 'NY.GDP.PCAP.PP.CD', 'SP.POP.TOTL', 'SI.POV.GINI',

'SE.SEC.CUAT.UP.ZS', 'NE.TRD.GNFS.ZS', 'GE.EST'],

dtype='object')

KOF dataset columns: Index(['code', 'country', 'year', 'KOFGI', 'KOFGIdf', 'KOFGIdj', 'KOFEcGI',

'KOFEcGIdf', 'KOFEcGIdj', 'KOFTrGI', 'KOFTrGIdf', 'KOFTrGIdj',

'KOFFiGI', 'KOFFiGIdf', 'KOFFiGIdj', 'KOFSoGI', 'KOFSoGIdf',

'KOFSoGIdj', 'KOFIpGI', 'KOFIpGIdf', 'KOFIpGIdj', 'KOFInGI',

'KOFInGIdf', 'KOFInGIdj', 'KOFCuGI', 'KOFCuGIdf', 'KOFCuGIdj',

'KOFPoGI', 'KOFPoGIdf', 'KOFPoGIdj'],

dtype='object')We observe a practical but important structural issue: the datasets do not use the same column name for the country code:

- World Bank uses

country_code - KOF uses

code - CEPII uses

iso3_o(exporter ISO3)

This is not just cosmetic. If we try to merge without first bringing these identifiers into a shared variable name, pandas will not be able to find the join key and will raise an error. Once we harmonise the identifier names (and ensure the identifier values are in compatible ISO3 format), we can safely merge and then diagnose coverage loss, which is the real substantive concern.

We therefore rename the identifier columns:

world_bank = world_bank.rename(columns={"country_code": "iso3_o"})

kof = kof.rename(columns={"code": "iso3_o"})3.1.2 Finding the overlapping years across CEPII, World Bank, and KOF

Now that identifiers are harmonised, we determine the set of candidate years for which all datasets contain data. We do this year-by-year using sets of exporter/country codes, because it allows us to reason transparently about coverage intersections.

trade_by_year = gravity.groupby("year")["iso3_o"].apply(set)

wb_by_year = world_bank.groupby("year")["iso3_o"].apply(set)

kof_by_year = kof.groupby("year")["iso3_o"].apply(set)We then compute the intersection of available years:

common_years = (

trade_by_year.index

.intersection(wb_by_year.index)

.intersection(kof_by_year.index)

)

common_yearsIndex([2017, 2018, 2019, 2020, 2021], dtype='int64', name='year')So 2017–2021 are feasible candidates from a purely data-availability perspective.

3.1.3 Coverage diagnostics by year (and why 2018 wins)

We now compute, for each common year:

- how many exporters/countries are present in CEPII (exporter side),

- how many countries are present in World Bank,

- how many countries are present in KOF, and

- how many countries survive the triple intersection.

overlap_df = pd.DataFrame({

"year": common_years,

"trade_countries": [len(trade_by_year[y]) for y in common_years],

"wb_countries": [len(wb_by_year[y]) for y in common_years],

"kof_countries": [len(kof_by_year[y]) for y in common_years],

"overlap_all_three": [

len(trade_by_year[y] & wb_by_year[y] & kof_by_year[y])

for y in common_years

]

})

overlap_df| year | trade_countries | wb_countries | kof_countries | overlap_all_three | |

|---|---|---|---|---|---|

| 0 | 2017 | 243 | 61 | 215 | 60 |

| 1 | 2018 | 243 | 72 | 215 | 71 |

| 2 | 2019 | 243 | 61 | 215 | 60 |

| 3 | 2020 | 243 | 59 | 215 | 58 |

| 4 | 2021 | 243 | 57 | 215 | 56 |

Interpretation (fully developed):

- CEPII exporter coverage is constant across these years (243 exporters), which reflects the dataset’s design: trade data tends to be far more “complete” in terms of country presence than macro and governance indicators.

- KOF coverage is also constant at 215 countries, which is large and fairly stable.

- The limiting dataset is clearly the World Bank extract you are using: it contains only 57–72 countries depending on year. That means that no matter how rich the trade data is, the modelling sample will inevitably be restricted to the subset of countries for which macro/outcome variables are available.

- The triple intersection is maximised in 2018 (71 countries). In other years it is closer to 56–60. That is a substantial difference when your entire modelling dataset is only ~70 observations: losing 10–15 countries would materially reduce statistical power, increase uncertainty in estimated relationships, and make model evaluation noisier and more sensitive to individual countries.

3.1.5 Selecting the modelling year

We choose 2018 because it provides the best balance of:

- maximum joint coverage (largest triple overlap),

- complete outcome observation,

- and substantive interpretability as a pre-pandemic baseline year.

analysis_year = 20183.2 Merging datasets

This part has three jobs, and it’s important to keep them distinct:

- Construct CEPII-derived trade structure indicators for the chosen year (2018).

- Merge trade indicators with KOF and World Bank (2018 slices).

- Report country counts before and after merging, and diagnose which countries are lost (and why that matters).

3.2.1 Recomputing CEPII-derived trade structure indicators for 2018

In Question 2, we constructed trade structure indicators using 2019 as an illustrative example. However, because we selected 2018 as the modelling year, we must recompute those indicators to ensure strict temporal alignment between predictors and outcome.

The logic is identical to Question 2. The only change is the reference year.

First, we isolate 2018 trade data:

gravity_year = gravity[gravity["year"] == analysis_year].copy()We inspect missingness:

gravity_year[["iso3_o", "iso3_d", "tradeflow_baci"]].isna().sum()Identifiers are complete. Trade flows contain missing values (there are fewer (about 700 fewer) missing values than in the 2019 set). Zeros are not explicitly coded.

We compute concentration conditional on observed flows. All trade structure indicators (HHI, diversification, effective partners) are computed conditional on observed bilateral flows. They therefore describe the structure of recorded trade, not necessarily total true trade.

gravity_year_obs = gravity_year.dropna(subset=["tradeflow_baci"]).copy()Calculating total exports

We start by computing total exports

total_exports_year = (

gravity_year_obs

.groupby("iso3_o")["tradeflow_baci"]

.sum()

.rename("total_exports")

)Computing export shares

We then compute export shares:

gravity_year_obs = gravity_year_obs.merge(

total_exports_year,

left_on="iso3_o",

right_index=True,

how="left"

)

gravity_year_obs["export_share"] = (

gravity_year_obs["tradeflow_baci"] /

gravity_year_obs["total_exports"]

)and check shares have been computed correctly:

gravity_year_obs.groupby("iso3_o")["export_share"].sum().describe()Export shares sum to one for every exporter (up to floating-point precision): this confirms that totals and shares were constructed correctly and that no incomplete exporter-level denominators were introduced.

Computing HHI

We then compute the Herfindahl-Hirschman Index for our dataset

hhi_year = (

gravity_year_obs

.groupby("iso3_o")["export_share"]

.apply(lambda x: (x**2).sum())

.rename("hhi")

)Combine indicators

We then compute indicators derived from the Herfindahl-Hirschman Index:

trade_structure_year = pd.concat(

[total_exports_year, hhi_year],

axis=1

)

trade_structure_year["diversification"] = 1 - trade_structure_year["hhi"]

trade_structure_year["effective_partners"] = 1 / trade_structure_year["hhi"]3.2.2 Coverage diagnostic: exporter-level missing bilateral flows (missing_flow_rate)

Because tradeflow_baci contains missing values, we need to assess whether measured export concentration may partly reflect incomplete bilateral coverage.

To do so, we compute, for each exporter, the fraction of potential bilateral observations in 2018 that have missing tradeflow values:

coverage_year = (

gravity_year

.assign(missing_flow=gravity_year["tradeflow_baci"].isna())

.groupby("iso3_o")["missing_flow"]

.mean()

.rename("missing_flow_rate")

)

trade_structure_year = trade_structure_year.merge(

coverage_year,

left_index=True,

right_index=True,

how="left"

)Importantly, missing_flow_rate measures the share of exporter–partner pairs for which no tradeflow value is recorded, not the share of export value that is missing.

Because international trade is highly skewed — with a small number of partners typically accounting for most trade value — a high missing-flow rate does not automatically imply that most export value is missing.

However, systematic absence of small bilateral flows can still mechanically affect concentration measures (HHI), since missing small flows inflate observed shares among recorded partners.

For this reason, we treat missing_flow_rate as a structural diagnostic and carry it forward explicitly rather than ignoring it.

To assess the stability and severity of bilateral trade coverage, we compare the exporter-level distribution of missing_flow_rate in 2018 and 2019 using:

- An overlaid histogram (with medians and quartile reference lines), and

- A threshold summary table showing the share of exporters exceeding key missingness cut-offs (20%, 40%, 60%, 80%).

Two separate questions guide these diagnostics:

- “Is exporter-level missingness high in absolute terms?”

- “Does it change materially between 2018 and 2019?”

The answer to the first is clearly yes: the typical exporter has roughly 45–47% of bilateral flows unrecorded. The answer to the second is no: differences between years are small and systematic rather than structural.

missing_flow_rate figure code

#| code-fold: true

x18 = trade_structure_year["missing_flow_rate"].dropna()

x19 = trade_structure_2019["missing_flow_rate"].dropna()

med18 = x18.median()

med19 = x19.median()

q18 = x18.quantile([0.25, 0.75])

q19 = x19.quantile([0.25, 0.75])

xbins = dict(start=0, end=1, size=0.05)

fig = go.Figure()

fig.add_trace(go.Histogram(

x=x18,

name="2018",

xbins=xbins,

bingroup="missing",

opacity=0.6,

marker_color="#1f77b4"

))

fig.add_trace(go.Histogram(

x=x19,

name="2019",

xbins=xbins,

bingroup="missing",

opacity=0.5,

marker_color="#ff7f0e"

))

# Quartile lines (lighter)

for q in q18:

fig.add_vline(x=q, line_color="#1f77b4", line_dash="dot", line_width=1)

for q in q19:

fig.add_vline(x=q, line_color="#ff7f0e", line_dash="dot", line_width=1)

# Median lines (thick)

fig.add_vline(

x=med18,

line_color="#1f77b4",

line_width=4,

annotation_text=f"2018 median ≈ {med18:.0%}",

annotation_position="top left",

annotation_font_color="#1f77b4"

)

fig.add_vline(

x=med19,

line_color="#ff7f0e",

line_width=4,

annotation_text=f"2019 median ≈ {med19:.0%}",

annotation_position="top right",

annotation_font_color="#ff7f0e"

)

fig.update_layout(

title=(

"Exporter-level missing bilateral trade flow rates (2018 vs 2019)"

"<br><sup>Median ≈ 45–47%; high missingness is common,</sup>""<br><sup>but distributions are very similar across years</sup>"

),

xaxis_title="Share of missing bilateral flows",

yaxis_title="Number of exporters",

barmode="overlay",

hovermode="x unified",

template="plotly_white"

)

fig.update_xaxes(range=[0,1], tickformat=",.0%")

fig.update_yaxes(tickformat=",")

fig.show()The overlaid histogram shows that:

- The distributions for both 2018 and 2019 are extremely similar in shape and location.

- Both years are centred around a median missingness of roughly 45–47%.

- The interquartile ranges overlap almost perfectly.

- There is a noticeable right tail in both years, with some exporters exhibiting very high missingness (above 80%), but these remain a minority.

Although visually very close, 2019 is slightly shifted to the right:

Mean missingness:

- 2018 ≈ 0.449

- 2019 ≈ 0.461

Median missingness:

- 2018 ≈ 0.446

- 2019 ≈ 0.466

This indicates that 2019 exhibits marginally higher missingness overall.

In terms of skewness:

- Both distributions are only mildly positively skewed.

- 2018 has slightly higher skew (≈ 0.16 vs ≈ 0.08), meaning its upper tail is marginally more pronounced relative to its centre.

- However, neither year shows extreme asymmetry.

Substantive takeaway

The key insight is not that missingness is “low” — it is not. Roughly half of bilateral flows per exporter are missing on average.

Rather, the important finding is that the pattern is structurally stable across years. There is no evidence of a sudden deterioration or dramatic structural shift between 2018 and 2019.

This stability supports treating 2018 as representative of the broader period for modelling purposes.

At this stage, we have country-level trade structure indicators for 2018.

thresholds = [0.2, 0.4, 0.6, 0.8]

summary = pd.DataFrame({

"threshold": thresholds,

"share_2018": [(trade_structure_year["missing_flow_rate"] > t).mean() for t in thresholds],

"share_2019": [(trade_structure_2019["missing_flow_rate"] > t).mean() for t in thresholds],

})

summary| threshold | share_2018 | share_2019 | |

|---|---|---|---|

| 0 | 0.2 | 0.852679 | 0.848214 |

| 1 | 0.4 | 0.562500 | 0.602679 |

| 2 | 0.6 | 0.272321 | 0.294643 |

| 3 | 0.8 | 0.049107 | 0.058036 |

The threshold table provides a more policy-relevant summary of how concentrated high missingness is.

| Threshold | Share 2018 | Share 2019 |

|---|---|---|

| > 20% | 85.3% | 84.8% |

| > 40% | 56.3% | 60.3% |

| > 60% | 27.2% | 29.5% |

| > 80% | 4.9% | 5.8% |

What the table tells us

Moderate incompleteness is essentially the baseline condition of the dataset. It is not a special-case edge phenomenon: more than 84% of exporters exceed 20% missing flows. That means any analysis built from recorded bilateral flows is inevitably being done on an incomplete graph of trade relationships. In practice, what varies by country is not whether missingness exists, but how severe it is.

The centre of the distribution implies “about half the bilateral matrix is missing” for a typical exporter. With 56–60% of exporters above 40% missingness, the median exporter is operating in a regime where roughly half of partner tradeflows are not recorded. That matters because concentration measures (HHI and derived metrics) are sensitive to whether “small partners” appear in the data.

A non-trivial minority experiences severe sparsity. Around 27–30% exceed 60% missingness. For these exporters, concentration indicators are more likely to be artefacts of which flows are recorded rather than purely reflective of real concentration. These exporters may deserve either explicit modelling of missingness, robustness checks, or at least interpretation caution.

Truly extreme sparsity exists but is rare. Only ~5% exceed 80% missingness. So while pathological cases exist, they do not dominate the sample.

Year-to-year comparison

At thresholds above 40%, 2019 is slightly worse than 2018. The differences are small but directionally consistent. That matters mainly because it supports the idea that missingness is structural rather than a sudden discontinuity across years. Selecting 2018 therefore does not appear to pick a “weird” year in terms of coverage.

Bottom line

The modelling dataset inherits an unavoidable structural limitation: the trade network is only partially observed for most exporters. However, because this incompleteness is stable across adjacent years and not dominated by a handful of extreme cases, we can proceed—provided we interpret trade structure variables as “structure of recorded trade flows” and we explicitly carry forward missing_flow_rate as a diagnostic (and potentially as a predictor).

3.2.3 Merging CEPII indicators with World Bank and KOF (2018 only)

At this point we have:

- A CEPII-derived, exporter-level dataset for 2018 (trade structure indicators +

missing_flow_rate) - KOF trade globalisation indices for 2018

- World Bank macro indicators (including the outcome) for 2018

We now form the modelling dataset, where each row is a country (exporter) in 2018.

world_bank_year = world_bank[world_bank["year"] == analysis_year].copy()

kof_year = kof[kof["year"] == analysis_year].copy()Country counts before merging (2018 only)

Before constructing the final modelling dataset, it is essential to quantify precisely which countries are lost when aligning CEPII trade data, KOF globalisation indices, and World Bank macro indicators for 2018.

We first examine country counts in each dataset:

set_cepii = set(gravity_year["iso3_o"].unique())

set_kof = set(kof_year["iso3_o"].unique())

set_wb = set(world_bank_year["iso3_o"].unique())

print("CEPII countries:", len(set_cepii))

print("KOF countries:", len(set_kof))

print("World Bank countries:", len(set_wb))

print("CEPII ∩ KOF:", len(set_cepii & set_kof))

print("CEPII ∩ WB:", len(set_cepii & set_wb))

print("KOF ∩ WB:", len(set_kof & set_wb))CEPII countries: 243

KOF countries: 215

World Bank countries: 72

CEPII ∩ KOF: 197

CEPII ∩ WB: 72

KOF ∩ WB: 71What this tells us is very specific:

- The “effective universe” of countries for modelling is the World Bank subset (72 countries). That is where the outcome lives, and without the outcome we cannot fit a supervised model.

- Every World Bank country in the 2018 subset appears in CEPII (CEPII ∩ WB = 72). So CEPII is not the bottleneck for the modelling sample; it will not reduce us below 72.

- The only reduction when requiring KOF as well is from 72 to 71 (KOF ∩ WB = 71). This means KOF is nearly complete relative to World Bank in 2018, but not perfectly.

This also highlights what is not captured by these counts:

- We see that many countries present in CEPII and KOF are missing from World Bank (because WB has only 72). Those are countries for which macro/outcome variables are not available in our extract. This is not a “merge mistake”; it is a data availability constraint that determines the scope of the modelling exercise.

Explicitly identifying lost ISO3 codes

We now inspect which countries are excluded when aligning datasets.

lost_from_kof_given_wb = sorted(list(set_wb - set_kof))

lost_from_wb_given_cepii = sorted(list(set_cepii - set_wb))

lost_from_wb_given_kof = sorted(list(set_kof - set_wb))

print("World Bank countries missing from KOF (WB \\ KOF):", lost_from_kof_given_wb)

print("CEPII exporters missing from World Bank (CEPII \\ WB):", lost_from_wb_given_cepii[:50], "...")

print("KOF countries missing from World Bank (KOF \\ WB):", lost_from_wb_given_kof[:50], "...")

print("Counts:")

print("WB \\ KOF:", len(lost_from_kof_given_wb))

print("CEPII \\ WB:", len(lost_from_wb_given_cepii))

print("KOF \\ WB:", len(lost_from_wb_given_kof))World Bank countries missing from KOF (WB \ KOF): ['ROU']

CEPII exporters missing from World Bank (CEPII \ WB):

['ABW', 'AFG', 'AGO', 'AIA', 'AND', 'ANT', 'ARE', 'ARG', 'ASM', 'ATG',

'AZE', 'BDI', 'BEN', 'BES', 'BGD', 'BHR', 'BHS', 'BIH', 'BLZ', 'BMU',

'BRB', 'BRN', 'BTN', 'BWA', 'CAF', 'CCK', 'CHL', 'CHN', 'CIV', 'CMR',

'COD', 'COG', 'COK', 'COM', 'CPV', 'CSK', 'CUB', 'CUW', 'CXR', 'CYM',

'DDR', 'DJI', 'DMA', 'DZA', 'EGY', 'ERI', 'ESH', 'ETH', 'FJI', 'FLK'] ...

KOF countries missing from World Bank (KOF \ WB):

['ABW', 'ADO', 'AFG', 'AGO', 'ARE', 'ARG', 'ATG', 'AZE', 'BDI', 'BEN',

'BGD', 'BHR', 'BHS', 'BIH', 'BLZ', 'BMU', 'BRB', 'BRN', 'BTN', 'BWA',

'CAF', 'CHL', 'CHN', 'CIV', 'CMR', 'COG', 'COM', 'CPV', 'CUB', 'CYM',

'DJI', 'DMA', 'DZA', 'EAS', 'ECS', 'EGY', 'ERI', 'ETH', 'FJI', 'FRO',

'FSM', 'GAB', 'GBR', 'GHA', 'GMB', 'GNQ', 'GRD', 'GRL', 'GTM', 'GUM'] ...

Counts:

WB \ KOF: 1

CEPII \ WB: 171

KOF \ WB: 144Interpretation of country losses

The asymmetry is striking:

- CEPII includes 243 exporters, but only 72 appear in the World Bank subset used here. That means 171 exporters are excluded purely due to macro/outcome data availability.

- Similarly, 144 KOF countries are excluded when aligning with the World Bank dataset.

Examining the ISO3 codes reveals several important structural patterns:

- Many excluded units are small territories (e.g., ABW, AIA, BMU, CYM, COK, FLK).

- Several fragile or lower-income states appear in the excluded lists (e.g., AFG, CAF, ERI, ETH, BDI).

- Some large emerging economies (e.g., CHN, ARG, ARE) also appear in the exclusion list — indicating that the World Bank extract used here is not globally comprehensive.

This implies that the modelling dataset is not a global sample of exporters, but rather a subset defined by macroeconomic reporting availability within the specific World Bank extract used.

Therefore, any conclusions drawn from the modelling exercise apply strictly to this 72-country subset and should not be interpreted as globally representative without qualification.

This is not a technical nuisance — it is a structural constraint that shapes external validity.

We now implement the dataset merges.

3.2.4 Merge construction (and why this merge design is chosen)

To merge the three datasets, we could choose between at least two principled strategies:

Strategy A: strict triple intersection (inner joins only)

This forces every observation to have trade indicators, KOF indicators, and World Bank indicators. The advantage is completeness. The disadvantage is that even a small amount of missingness in one dataset can drop countries entirely.

Strategy B: anchor on outcome availability, preserve coverage, and treat predictor missingness explicitly

This is what we do. The logic is:

- We must have the outcome (World Bank) for modelling, so the modelling sample is anchored there.

- Trade indicators are fully observed for the exporters we keep.

- If KOF is missing for one country, we prefer to keep the country and treat KOF as a missing predictor rather than drop the entire observation.

This strategy yields a larger modelling sample and forces us to confront missingness transparently rather than hiding it via sample deletion.

We therefore implement:

- left join trade → KOF

- left join result → World Bank

- then filter to outcome observed

model_data_full = (

trade_structure_year

.reset_index()

.merge(

kof_year[["iso3_o", "KOFTrGIdf", "KOFTrGIdj"]],

on="iso3_o",

how="left"

)

.merge(

world_bank_year,

on="iso3_o",

how="left"

)

)We restrict the data to data with observed outcome:

model_data = model_data_full[

model_data_full["NY.ADJ.NNAT.GN.ZS"].notna()

].copy()

model_data["iso3_o"].nunique()72Interpretation:

We obtain 72 modelling countries in 2018. This is exactly the World Bank coverage for the year, which reinforces the earlier conclusion: World Bank is the binding constraint on sample size in this setup.

3.3 Exploring the combined dataset

This part is about understanding what we have constructed before modelling:

- Where is missingness located?

- How strongly do the predictors relate to each other (overlap/redundancy)?

- Do trade structure indicators provide distinct information from trade openness and globalisation?

3.3.1 Missing values across variables (post-merge)

We compute missingness rates:

model_data.isna().mean().sort_values(ascending=False)KOFTrGIdf 0.013889

KOFTrGIdj 0.013889

iso3_o 0.000000

NY.GDP.TOTL.RT.ZS 0.000000

NE.TRD.GNFS.ZS 0.000000

SE.SEC.CUAT.UP.ZS 0.000000

SI.POV.GINI 0.000000

SP.POP.TOTL 0.000000

NY.GDP.PCAP.PP.CD 0.000000

NY.ADJ.NNAT.GN.ZS 0.000000

year 0.000000

total_exports 0.000000

country_name 0.000000

missing_flow_rate 0.000000

effective_partners 0.000000

diversification 0.000000

hhi 0.000000

GE.EST 0.000000

dtype: float64For visual inspection:

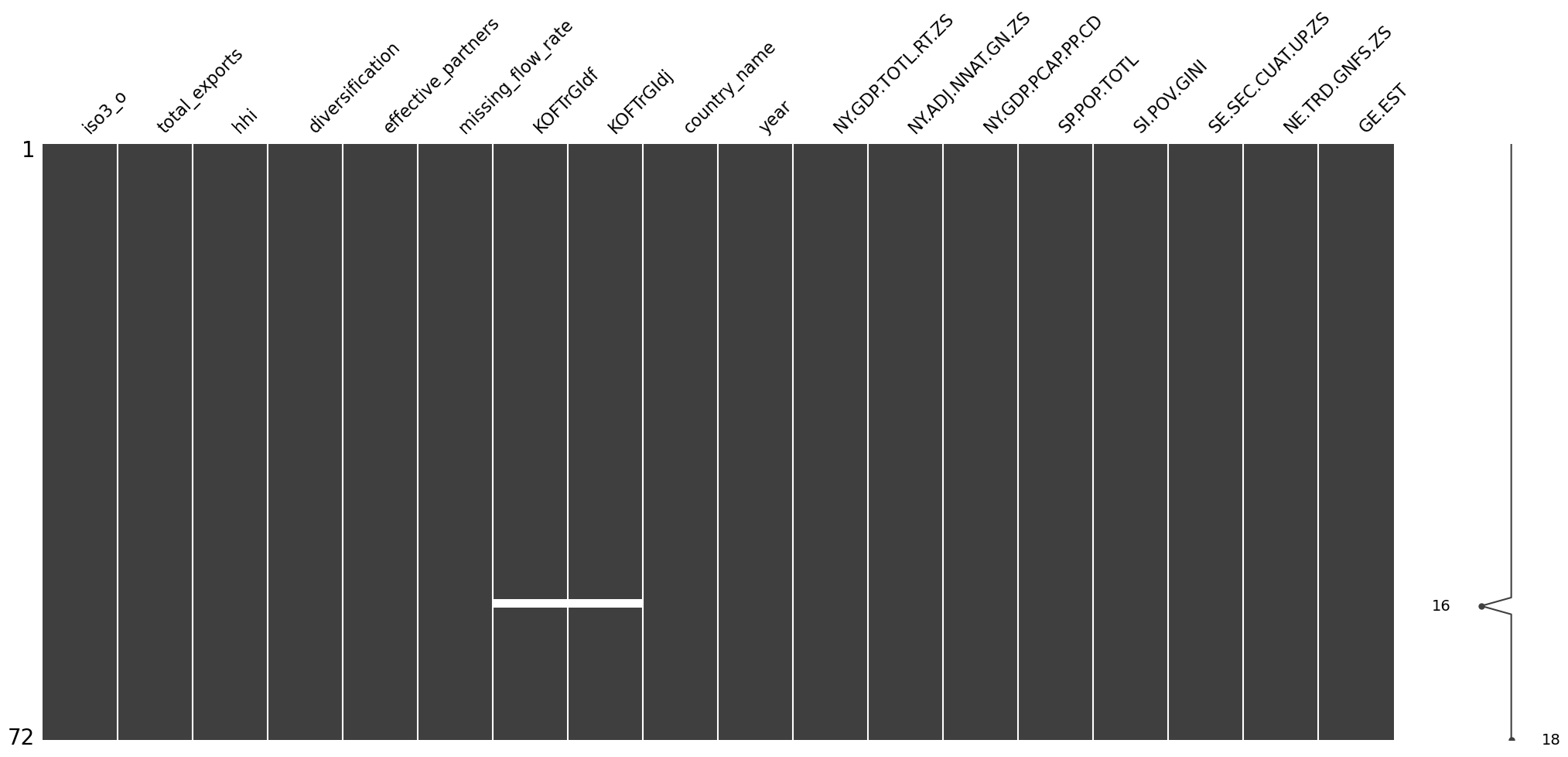

msno.matrix(model_data)

Interpretation:

The merged dataset is unusually clean for cross-country macro work:

- The outcome (

NY.ADJ.NNAT.GN.ZS) is fully observed in the modelling sample. - All CEPII-derived trade structure variables are fully observed including

missing_flow_rate. This is important: it means we can treat trade structure and trade coverage as first-class pieces of information rather than losing observations. - Missingness is confined to the KOF trade globalisation sub-indices and is perfectly aligned across de facto and de jure, suggesting a shared mechanism (a country missing from that part of KOF in that year), not random measurement noise.

This matters for modelling later because “a little bit of missingness” can still create leakage or distort evaluation if it is handled outside a train/test framework. That is why imputation is deferred to Question 4.

3.3.2 Correlation structure of the merged dataset

To understand redundancy, overlap, and potential multicollinearity among predictors, we compute the full correlation matrix of the merged dataset (excluding identifiers).

corr = model_data.drop(columns=['iso3_o','year','country_name']).corr()

corr| total_exports | hhi | diversification | effective_partners | missing_flow_rate | KOFTrGIdf | KOFTrGIdj | NY.GDP.TOTL.RT.ZS | NY.ADJ.NNAT.GN.ZS | NY.GDP.PCAP.PP.CD | SP.POP.TOTL | SI.POV.GINI | SE.SEC.CUAT.UP.ZS | NE.TRD.GNFS.ZS | GE.EST | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| total_exports | 1.000000 | -0.076026 | 0.076026 | 0.177872 | -0.232060 | -0.120466 | 0.268683 | -0.140503 | -0.000070 | 0.396331 | 0.566820 | -0.013330 | 0.244405 | -0.130540 | 0.397097 |

| hhi | -0.076026 | 1.000000 | -1.000000 | -0.682510 | 0.382222 | -0.299974 | -0.359129 | 0.424416 | -0.012133 | -0.246795 | -0.088752 | 0.129687 | -0.245064 | -0.106609 | -0.316478 |

| diversification | 0.076026 | -1.000000 | 1.000000 | 0.682510 | -0.382222 | 0.299974 | 0.359129 | -0.424416 | 0.012133 | 0.246795 | 0.088752 | -0.129687 | 0.245064 | 0.106609 | 0.316478 |

| effective_partners | 0.177872 | -0.682510 | 0.682510 | 1.000000 | -0.311318 | 0.282002 | 0.350882 | -0.252902 | 0.009655 | 0.170267 | 0.215417 | -0.204801 | 0.206916 | 0.058282 | 0.225682 |

| missing_flow_rate | -0.232060 | 0.382222 | -0.382222 | -0.311318 | 1.000000 | -0.218427 | -0.592778 | 0.389790 | 0.083723 | -0.578085 | 0.020145 | 0.091286 | -0.406794 | -0.152807 | -0.607236 |

| KOFTrGIdf | -0.120466 | -0.299974 | 0.299974 | 0.282002 | -0.218427 | 1.000000 | 0.601533 | -0.433952 | 0.028084 | 0.362522 | -0.498314 | -0.503678 | 0.544180 | 0.707312 | 0.463385 |

| KOFTrGIdj | 0.268683 | -0.359129 | 0.359129 | 0.350882 | -0.592778 | 0.601533 | 1.000000 | -0.617680 | -0.111703 | 0.692343 | -0.111290 | -0.379753 | 0.700425 | 0.437056 | 0.801711 |

| NY.GDP.TOTL.RT.ZS | -0.140503 | 0.424416 | -0.424416 | -0.252902 | 0.389790 | -0.433952 | -0.617680 | 1.000000 | 0.107085 | -0.366531 | 0.046809 | 0.041881 | -0.194412 | -0.290767 | -0.444546 |

| NY.ADJ.NNAT.GN.ZS | -0.000070 | -0.012133 | 0.012133 | 0.009655 | 0.083723 | 0.028084 | -0.111703 | 0.107085 | 1.000000 | 0.057245 | -0.031117 | 0.080798 | -0.089439 | 0.105285 | 0.028331 |

| NY.GDP.PCAP.PP.CD | 0.396331 | -0.246795 | 0.246795 | 0.170267 | -0.578085 | 0.362522 | 0.692343 | -0.366531 | 0.057245 | 1.000000 | -0.056758 | -0.348773 | 0.576358 | 0.532532 | 0.880478 |

| SP.POP.TOTL | 0.566820 | -0.088752 | 0.088752 | 0.215417 | 0.020145 | -0.498314 | -0.111290 | 0.046809 | -0.031117 | -0.056758 | 1.000000 | 0.244351 | -0.109504 | -0.358983 | -0.072119 |

| SI.POV.GINI | -0.013330 | 0.129687 | -0.129687 | -0.204801 | 0.091286 | -0.503678 | -0.379753 | 0.041881 | 0.080798 | -0.348773 | 0.244351 | 1.000000 | -0.463580 | -0.397451 | -0.412708 |

| SE.SEC.CUAT.UP.ZS | 0.244405 | -0.245064 | 0.245064 | 0.206916 | -0.406794 | 0.544180 | 0.700425 | -0.194412 | -0.089439 | 0.576358 | -0.109504 | -0.463580 | 1.000000 | 0.366140 | 0.653367 |

| NE.TRD.GNFS.ZS | -0.130540 | -0.106609 | 0.106609 | 0.058282 | -0.152807 | 0.707312 | 0.437056 | -0.290767 | 0.105285 | 0.532532 | -0.358983 | -0.397451 | 0.366140 | 1.000000 | 0.395632 |

| GE.EST | 0.397097 | -0.316478 | 0.316478 | 0.225682 | -0.607236 | 0.463385 | 0.801711 | -0.444546 | 0.028331 | 0.880478 | -0.072119 | -0.412708 | 0.653367 | 0.395632 | 1.000000 |

To visualise the structure more clearly, we produce a heatmap.

fig = px.imshow(

corr,

color_continuous_scale="RdBu_r", # red = positive, blue = negative

zmin=-1,

zmax=1,

text_auto=True,

title="Correlation heatmap of merged modelling dataset (2018)"

)

fig.update_layout(width=1000, height=900)

fig.show()Interpretation of the correlation structure

Several substantive patterns emerge.

1. Trade structure indicators are mechanically related

hhianddiversificationhave a perfect correlation of −1 because diversification is defined as (1 - ).effective_partnersis strongly negatively correlated withhhi(≈ −0.68), as expected given its inverse construction.

These should not be included simultaneously in a linear model, as they encode the same concentration concept.

2. Missing flow rate is systematically related to development and governance

missing_flow_rate is:

- Strongly negatively correlated with governance (

GE.EST≈ −0.61), - Strongly negatively correlated with GDP per capita (

NY.GDP.PCAP.PP.CD≈ −0.58), - Strongly negatively correlated with KOF de jure trade globalisation (

KOFTrGIdj≈ −0.59).

This is an important substantive insight: missing trade flows are not random measurement error. They appear systematically higher in countries with weaker institutions and lower income levels.

Therefore, missing_flow_rate may partly proxy state capacity or reporting infrastructure, and ignoring it could bias interpretation of trade structure indicators.

3. Trade openness and KOF de facto globalisation overlap strongly

NE.TRD.GNFS.ZSandKOFTrGIdfcorrelate at ≈ 0.71.

Both measure realised trade integration, so this high correlation is conceptually coherent. Including both in a regression may introduce redundancy rather than independent explanatory content.

4. Governance and GDP per capita are tightly linked

GE.ESTandNY.GDP.PCAP.PP.CDcorrelate at ≈ 0.88.

This is a classic development pattern: richer countries tend to have stronger governance scores. Including both without consideration may introduce multicollinearity.

5. The outcome shows weak simple correlations

NY.ADJ.NNAT.GN.ZS exhibits relatively small pairwise correlations with most predictors.

This suggests:

- Growth in this cross-section is influenced by multiple interacting factors.

- No single predictor dominates in simple bivariate terms.

- Multivariate modelling will be required to assess combined explanatory power.

3.4 Exploring the outcome variable

This final part is exploratory and is about understanding the target we are trying to predict: adjusted net national income growth.

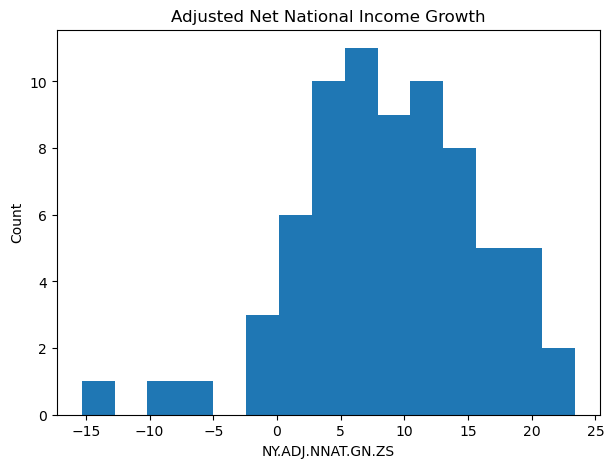

We first look at the numeric distribution summary:

model_data["NY.ADJ.NNAT.GN.ZS"].describe()count 72.000000

mean 8.739472

std 7.170640

min -15.336925

25% 3.970531

50% 8.817603

75% 13.571349

max 23.386105

Name: NY.ADJ.NNAT.GN.ZS, dtype: float64Interpretation (fully expanded):

- The outcome spans a wide range: from about −15% to +23%, which is substantial variation for a growth measure across countries in a single year.

- The distribution centre is around 8–9% (mean ≈ 8.7, median ≈ 8.8), suggesting that in 2018 many countries in this sample experienced positive adjusted net national income growth.

- The standard deviation (~7.2) is large relative to the mean, implying that cross-country heterogeneity is strong.

- The lower tail includes a small number of clearly negative-growth cases, which are substantively important because they can influence model fit, residual structure, and coefficient sensitivity in a small sample.

We then visualise the shape of the distribution:

plt.figure(figsize=(7,5))

plt.hist(model_data["NY.ADJ.NNAT.GN.ZS"], bins=15)

plt.title("Adjusted Net National Income Growth")

plt.xlabel("NY.ADJ.NNAT.GN.ZS")

plt.ylabel("Count")

plt.show()

From the plotted shape, the distribution appears broadly unimodal, with some tail mass on both sides. It does not look like a strictly log-normal or multiplicative process that would immediately force a log transform. Since the outcome takes negative values, a log transform is also not directly available without shifting, which would itself introduce interpretability complications.

At this stage, we therefore do not apply transformations. The right way to decide later is based on modelling diagnostics (residual patterns, heteroskedasticity, and whether error variance grows with fitted values), which belongs in Question 4 once we have a proper train/test setup.

Question 4 – Predictive Modelling

We now build predictive models to explain cross-country variation in adjusted net national income growth (2018) using the trade structure, trade integration, and macro-institutional variables constructed in Question 3.

The modelling objective is predictive rather than causal. Our focus is therefore on:

- Out-of-sample predictive performance

- Stability of coefficient estimates

- Economic interpretability

4.1 Baseline Linear Model

4.1.1 Train–Test Split

The dataset contains 72 countries. The number of predictors under consideration is substantial relative to sample size, and growth rates exhibit wide dispersion (approximately −15% to +23%).

If the model were estimated and evaluated on the same data, the resulting performance metrics would reflect in-sample fit rather than predictive capacity. This is particularly problematic in small cross-sectional datasets because:

- Ordinary least squares (OLS) can easily overfit noise.

- Coefficient estimates may be unstable.

- Extreme observations can disproportionately influence fit.

- Apparent explanatory power may not generalise.

To obtain an unbiased estimate of predictive performance, we partition the data into training and test sets:

X = model_data.drop(columns=["iso3_o", "country_name", "year", "NY.ADJ.NNAT.GN.ZS"])

y = model_data["NY.ADJ.NNAT.GN.ZS"]

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.2, random_state=42

)

len(X_train), len(X_test)Training sample: 57 countries Test sample: 15 countries

The test set represents approximately 20% of the available data. Because it contains only 15 observations, evaluation metrics will be sensitive to individual countries. A single extreme residual can materially affect R² and RMSE. This must be borne in mind when interpreting results.

All preprocessing steps (imputation, scaling, feature selection diagnostics) are performed using training data only.

Why 80/20 rather than 70/30?

With 72 total observations: